Prosegur Cash o Prosegur Cia: Parte I - Príncipe o mendigo (English version at the end)

Prosegur Cash o Prosegur Cia: Parte I - Príncipe o mendigo (English version at the end)

“Cuando el sabio señala la luna, el necio mira el dedo”. Confucio.

Gubel, sociedad controlada por Helena Revoredo, y accionista mayoritaria de Prosegur Cia de Seguridad SA (Prosegur Cia), lanzó el 15 de noviembre de 2023 una Oferta Pública de Adquisición (OPA) voluntaria sobre un 15% del capital de Prosegur Cia.

La familia Revoredo cuenta con un ~60% del capital y con este movimiento se situaría con un ~75% de la compañía, tras pagar €150m, que supone una prima del 27% sobre el precio de cierre del día anterior.

A pesar de que, el precio de la OPA es de 1.83€, hoy Prosegur Cia cotiza a un precio de 1.74€, lo que equivaldría a una rentabilidad vía arbitraje de ~5%. Lo que nosotros llamamos la ganancia del mendigo.

Sin embargo, es posible que haya muchos granos de cacao esperando tras este movimiento.

Se ha especulado que este podría ser un primer paso para realizar una OPA de exclusión sobre Prosegur Cash, la compañía del grupo dedicada principalmente al transporte y a la gestión de efectivo.

Actualmente, Prosegur Cia es dueña del 79% de Prosegur Cash y tras sacarla a bolsa a un precio de 2€ en 2017, la familia fundadora podría aprovechar que “Cash” cotiza en sus mínimos históricos para intentar lanzar una exclusión por un canje de las acciones de Prosegur Cia, tras la OPA parcial lanzada por la familia y evitar así una pérdida de control por dilución.

De ser así, y teniendo en cuenta que Prosegur Cash está cotizando a un precio de 0.47€, no descartaríamos una oferta con un canje equivalente a un precio de 0.60€-0.65€ por acción de Prosegur Cash, es decir, ganar entre un 30%-40% en tan solo unos meses.

El mendigo: Comprar Prosegur Cia

A día de hoy habría una posibilidad de obtener un beneficio mínimo de un 5%, siempre y cuando la OPA parcial lanzada en noviembre a 1.83€ salga adelante. Las últimas noticias confirman que la OPA fue registrada el 12 de diciembre y que el 21 de diciembre fue admitida a trámite por la CNMV. A pesar de esto, la aceptación de la OPA no está garantizada. La principal objeción por parte de la CNMV podría venir con respecto al precio de la OPA.

La ley de OPAs contempla que el precio ofertado por Gubel debe ser el más alto de entre:

La media de los últimos 6 meses de cotización: Que estaría por debajo de 1.83€.

El valor en libros de Prosegur Cia: Que estaría por debajo de 1.83€.

El precio pagado por Gubel en compras de acciones en los últimos 12 meses.

Al respecto de la tercera cláusula que hace referencia a las compras de acciones de los últimos 12 meses, la compañía difundió en un comunicado oficial la siguiente información:

Las únicas adquisiciones de acciones de Prosegur Cia realizadas durante los 12 meses previos a este anuncio por el Oferente, las compañías pertenecientes al grupo de sociedades del que el Oferente es parte o controladas, directa o indirectamente, por doña Helena Revoredo Delvecchio, los administradores del Oferente o, según el leal saber y entender del Oferente, los administradores de las restantes sociedades anteriormente mencionadas que hayan sido designados a instancias del Oferente, son las siguientes:

• Compra en mercado de un total de 550.000 acciones de Prosegur Cia por Gubel a un precio máximo de 1,5996 euros por acción.

• Adquisición por don Christian Gut Revoredo, en su condición de consejero ejecutivo de Prosegur Cia, el 21 de diciembre de 2022, de 552.301 acciones de Prosegur Cia como consecuencia de la liquidación de plan de incentivo a largo plazo denominado “Plan Global Optimum”, con un valor unitario de 1,72 euros por acción. Además, sus personas estrechamente vinculadas compraron en mercado un total de 1.000.000 de acciones a un precio máximo de 1,8100 euros por acción.

• Compra en mercado de 350.446 acciones de Prosegur Cia por don Germán Gut Revoredo a un precio máximo de 1,6209 euros por acción.

• Compra en mercado de 605.441 acciones por parte de doña Bárbara Gut Revoredo y 421.895 por parte de sus personas estrechamente vinculadas, a un precio máximo de 1,8700 euros por acción.

¡Bingo!, Bárbara Gut Revoredo, una de las principales accionistas de Gubel e hija de Helena Revoredo, habría realizado una compra de ~1.000.000 de acciones a un precio máximo de 1.87€ durante los 12 meses previos a la oferta de OPA parcial.

Entendemos que (aunque no podemos asegurar porque no somos abogados), según la ley, habría alguna posibilidad de que la CNMV exigiera a Gubel incrementar el precio de la OPA a 1.87€, que elevaría la posible rentabilidad por arbitraje a un 7%.

En cualquier caso, para ser más conservadores tomaríamos 1.83€ como el precio más probable aceptado por la CNMV.

Periodo de aceptación y mecanismo de prorrateo:

Como en todo arbitraje en OPAs parciales, nos encontramos con dos “handicaps”:

1. El periodo de aceptación: ¿Cuánto tiempo va a estar el dinero parado?

2. La oferta es solo por el 15% del capital: ¿Qué pasa si acude todo el mundo?

Periodo de aceptación y liquidación:

El periodo de aceptación estimado es de entre dos a tres meses.

Como referente más cercano tendríamos la OPA parcial de FCC lanzada a finales de junio de 2023 y que fue liquidada en diciembre. No obstante, habría que tener en cuenta que el proceso se dio en los meses de vacaciones e incluía la convocatoria para aprobación formal en junta de accionistas y el visto bueno de la CNMV.

Prorrateo:

Al ser la OPA solo por el 15% y teniendo en cuenta que Gubel controla el 60% de la compañía, habría otro 25% restante que podría acudir a la oferta, en cuyo caso se debería producir un prorrateo.

Sin embargo, hay una ventaja legal para los pequeños inversores: la ley de OPAs establece que para estos casos, el 25% de la oferta se repartirá de forma igualitaria entre el número de peticiones independientemente de la cantidad de acciones solicitadas.

Nota: el siguiente tipo de operativa solo funciona bien con brokers españoles y algunos puntuales extranjeros como Interactive Brokers.

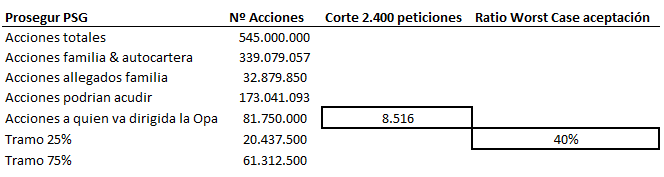

En números supone: El 25% de la oferta total (81.754.030 acciones) son 20.438.508 de acciones que se tienen que repartir entre el número de solicitudes de forma igualitaria. Según la información del siguiente link: (https://www.eleconomista.es/mercados-cotizaciones/noticias/8673719/10/17/El-91-de-los-accionistas-invierte-en-empresas-con-consejo-de-mantener.html, Prosegur contaba en 2017 con 2.400 accionistas, si asumimos que continúa habiendo ~2.400 accionistas que solicitan acudir a la OPA, a todo el mundo, independientemente de la cantidad que pida, le van a tomar un mínimo de 8.500 acciones a 1.83€. (20.438.528/2.400).

Esto significa que un “retail” que acuda, supongamos con una cantidad humilde de 5.000€/10.000€, tiene una probabilidad alta de que le compren todas sus acciones. En cambio, esto no sería así para un cliente institucional o un fondo que acuda con millones de euros, porque en este caso asumiendo 2.400 peticiones, solo le tomarían igualmente 8.500 acciones en el primer tramo de corte lineal del 25%

¿Qué pasaría si voy con 15.000 acciones y el corte es de 8.500 acciones?

El resto de acciones que tomarían es el resultado de multiplicar el porcentaje final de aceptación por el número de acciones restantes.

Fuente: Estados financieros de Prosegur CIA

La oferta total es por ~81m de acciones y tras el reparto lineal del 25%, quedarían ~60m de acciones para repartir por prorrateo. Suponiendo que hay ~173m total de acciones susceptibles de acudir excluyendo las acciones de la familia y allegados y la autocartera, nos quedarían un ratio máximo de aceptación del 40%.

Implica que, para las 6.500 acciones restantes, si el porcentaje de aceptación es del 40%, solo serían aceptadas en la oferta otras 2.600 acciones más por prorrateo.

Habría que tener en cuenta que los números se han realizado a partir del número de accionistas de 2017 y asumiendo que acude todo el “float”. La realidad es que Prosegur Cia está cotizando en mínimos de 2005, por lo que es posible que muchos accionistas a ese precio sigan en pérdidas y decidan no acudir.

En relación a los fondos institucionales, que son clave para el segundo tramo del prorrateo, dudamos que acudan en masa ya que el precio al que los analistas valoran Prosegur Cia estaría entre 2€ y 3.50€.

Si se repite la experiencia reciente en FCC, la OPA parcial de Prosegur Cia podría no completarse. Dicha OPA parcial estaba dirigida al 7% y finalmente acudió solo el 4.5%.

El príncipe: Comprar acciones de Prosegur Cash (CASH)

Algunas quinielas apostarían a que la OPA parcial a Prosegur Cia es parte de otro movimiento corporativo más importante.

En relación a la OPA parcial lanzada para acaparar el 75% de Prosegur Cia, hay algunas dudas de por qué drenar de liquidez a la acción, cuando la familia ya tiene el control de la compañía con el actual porcentaje del ~60%. Aunque no dudamos que esta oferta haya sido fruto de la oportunidad que brinda los recientes mínimos de Prosegur Cia, habría otra posibilidad más interesante: El “deslistado” definitivo del 20% cotizado de Prosegur Cash, compañía propiedad de Prosegur Cia en un ~80%.

Prosegur Cash es la filial dedicada al tránsito y gestión del efectivo, negocio de poco crecimiento, pero con un posicionamiento líder en algunos países de Latinoamérica, donde la tasa de bancarización continúa siendo baja.

Prosegur Cash salió a bolsa mediante una IPO en 2017 a un precio de 2€, en la que Prosegur Cia pretendía poner en valor esta división altamente rentable. Así, Gut Revoredo declaró:

“Estamos convencidos de que [Prosegur Cash] será una de las empresas más importantes del mercado”

Siete años después, la compañía se encuentra cotizando en 0.47€, un 77% por debajo del precio de salida a bolsa. Y esto a pesar, de que las ventas no han parado de crecer. Pero en esta cuestión entraremos más en detalle en la segunda parte de esta historia, que dejamos para otra publicación.

Continuamos…

Habiendo fracasado el movimiento de puesta en valor de Prosegur Cash, parecería que tiene sentido y crearía valor para Prosegur Cia una adquisición de las acciones de Prosegur Cash por menos de la mitad del precio al que consiguieron vender en la colocación de 2017.

Además, creemos que hay bastantes posibilidades de que la verdadera intención final de la OPA parcial a Prosegur Cia tenga la finalidad de facilitar un canje de acciones de Prosegur Cia por todas las acciones de Prosegur Cash en manos ajenas, sin que la familia pierda el control del grupo y devuelva la liquidez drenada a la acción de Prosegur Cia.

¿Como se podría orquestar la operación?

Si suponemos que la familia intenta deslistar Prosegur Cash pagando una prima del 35% (que suele ser lo normal en este tipo de operaciones), los números serían los siguientes:

Para deslistar las ~268m de acciones de Prosegur Cash con una prima del 35% la ecuación de canje tras el precio de la OPA parcial sería de 2.88 acciones de Prosegur Cash por cada una de Prosegur Cia.

¿Cuantas acciones tendría que emitir Prosegur Cia para deslistar Prosegur Cash al 35% de prima?

Una vez llevada a cabo la OPA parcial a Prosegur Cia por parte de Gubel, el porcentaje de acciones en mano de la familia con respecto a Prosegur Cia pasaría ser >75%.

Posteriormente, para lanzar una OPA por Prosegur Cash con prima, Prosegur Cia tendría que emitir 93.208.432 acciones nuevas.

¿Cómo quedaría el porcentaje de la familia tras la dilución?

Recapitulando:

Asumimos que la OPA parcial a Prosegur Cia se cierra en 1.83€ y con este paso la familia incrementa el peso del 62% al 77%.

Posteriormente Prosegur Cia podría lanzar una OPA de exclusión a Prosegur Cash con una prima del 35% a través de un canje de 2.88 acciones de Prosegur Cash por cada acción de Prosegur Cia.

Prosegur Cia emitiría 93m de acciones, lo que supondría una dilución de la familia del ~77% al ~66%, lo que llevaría a seguir manteniendo el control de Prosegur Cia de manera holgada e incluso tendría margen para elevar la oferta.

La familia consigue excluir a Prosegur Cash a un precio con prima de 0.63€, un 70% por debajo del precio de colocación en 2017.

¿Por qué no realizar la exclusión de Prosegur Cash directamente a través de una compra por parte de Prosegur Cia sin la OPA parcial previa de la familia?

Si se realiza con acciones: la familia se diluiría y estaría cerca de perder el control.

Si se realiza con deuda: se compromete el balance en un momento en el que el endeudamiento se sitúa en €1.05b. Adicionalmente, si incluimos la posible compra de Prosegur Cash, la deuda neta se incrementaría a €1.2b, un ratio algo por encima a 2.5x Deuda Neta / EBITDA.

Finalmente, ¿cuál sería la valoración de Prosegur Cia y Prosegur Cash en el caso de que no saliese la operación y nos quedáramos atrapados?

Esto es material para otra entrada…próximamente en la segunda parte de esta historia.

¡Hasta la próxima!

Prosegur Cash or Prosegur Cia: Part I - The prince and the Pauper

When a Wise Man Points at the Moon, The Fool Looks at the Finger. Confucio

Gubel, a company controlled by Helena Revoredo and majority shareholder of Prosegur Cia de Seguridad SA (Prosegur Cia), launched a voluntary public takeover bid (OPA) on November 15, 2023, for 15% of Prosegur Cia's capital.

The Revoredo family holds approximately 60% of the capital, and with this move, they would increase their stake to around 75% in the company, paying €150 million, representing a 27% premium over the previous day's closing price.

Despite the OPA price being €1.83, Prosegur Cia is currently trading at €1.74, offering an arbitrage return of approximately 5%, what we refer to as the "beggar's gain."

However, there might be more to this move than meets the eye.

There is speculation that this could be a preliminary step towards an exclusion takeover bid for Prosegur Cash, a company within the group primarily dedicated to transportation and cash management.

Currently, Prosegur Cia owns 79% of Prosegur Cash, and after its IPO at €2 in 2017, the founding family could capitalize on "Cash" trading at historic lows. They might attempt an exclusion bid by exchanging Prosegur Cia's shares, following the partial OPA launched by the family, thereby avoiding a loss of control through dilution.

If this scenario unfolds, considering Prosegur Cash is trading at €0.47, we wouldn't rule out an offer with an exchange equivalent to a price of €0.60-0.65 per Prosegur Cash share, implying a gain of 30%-40% in just a few months.

The Pauper: Buying Prosegur Cia

As of today, there would be a possibility of obtaining a minimum profit of 5%, provided that the partial takeover bid launched in November at €1.83 moves forward. The latest news confirms that the bid was registered on December 12 and was admitted for processing by the CNMV on December 21. However, the acceptance of the bid is not guaranteed. The CNMV's main objection could concern the bid price.

The takeover bid law stipulates that the price offered by Gubel must be the highest of:

The average of the last 6 months of trading: Which would be below €1.83.

Prosegur Cia's book value: Which would be below €1.83.

The price paid by Gubel in share purchases over the last 12 months.

Regarding the third clause referring to share purchases over the last 12 months, the company released the following information in an official statement:

The only acquisitions of Prosegur Cia shares made by the Offeror during the 12 months prior to this announcement, by companies belonging to the group of companies of which the Offeror is part or controlled, directly or indirectly, by Ms. Helena Revoredo Delvecchio, the Offeror's directors, or, according to the Offeror's best knowledge and understanding, the directors of the other aforementioned companies who have been appointed at the behest of the Offeror, are as follows:

Market purchase of a total of 550,000 Prosegur Cia shares by Gubel at a maximum price of €1.5996 per share.

Acquisition by Mr. Christian Gut Revoredo, in his capacity as executive director of Prosegur Cia, on December 21, 2022, of 552,301 Prosegur Cia shares as a result of the settlement of a long-term incentive plan called "Global Optimum Plan," with a unit value of €1.72 per share. In addition, his closely related persons purchased a total of 1,000,000 shares in the market at a maximum price of €1.81 per share.

Market purchase of 350,446 Prosegur Cia shares by Mr. Germán Gut Revoredo at a maximum price of €1.6209 per share.

Market purchase of 605,441 shares by Mrs. Bárbara Gut Revoredo and 421,895 by her closely related persons, at a maximum price of €1.87 per share.

Bingo! Barbara Gut Revoredo, one of the main shareholders of Gubel and daughter of Helena Revoredo, would have made a purchase of approximately 1,000,000 shares at a maximum price of €1.87 during the 12 months prior to the partial takeover bid offer.

We understand that (although we cannot guarantee because we are not lawyers), according to the law, there might be a possibility that the CNMV could demand that Gubel increase the takeover bid price to €1.87, which would raise the potential arbitrage return to 7%.

In any case, to be more conservative, we would take €1.83 as the most likely price accepted by the CNMV.

Acceptance period and proration mechanism:

As in all arbitrage in partial takeover bids, we encounter two handicaps:

The acceptance period: How long will the money be tied up?

The bid is only for 15% of the capital: What happens if everyone participates?

Acceptance and settlement period:

The estimated acceptance period is between two to three months.

The closest reference we would have is the partial bid for FCC launched at the end of June 2023, which was settled in December. However, it should be noted that the process took place during the holiday months and included the call for formal approval at the shareholders' meeting and approval by the CNMV.

Proration:

Since the bid is only for 15%, and considering that Gubel controls 60% of the company, there would be another 25% remaining that could participate in the bid, in which case proration would occur.

However, there is a legal advantage for small investors: the takeover bid law states that in these cases, 25% of the bid will be distributed equally among the number of requests regardless of the number of shares requested.

Note: The following type of operation works well only with Spanish brokers and some specific foreign brokers such as Interactive Brokers.

In numbers, this means: 25% of the total bid (81,754,030 shares) is 20,438,508 shares that must be distributed among the number of requests equally. According to information from the following link: (https://www.eleconomista.es/mercados-cotizaciones/noticias/8673719/10/17/El-91-de-los-accionistas-invierte-en-empresas-con-consejo-de-mantener.html), Prosegur had 2,400 shareholders in 2017. Assuming that there are still approximately 2,400 shareholders who request to participate in the bid, everyone, regardless of the amount requested, will be allocated a minimum of 8,500 shares at €1.83. (20,438,528/2,400).

This means that a "retail" investor who participates, let's say with a modest amount of €5,000/€10,000, has a high probability of having all their shares bought. However, this wouldn't be the case for an institutional client or a fund investing with millions of euros. Assuming 2,400 requests, they would still be allocated only 8,500 shares in the initial linear cutoff of 25%.

What would happen if I go in with 15,000 shares and the cutoff is 8,500 shares?

The remaining shares they would receive depend on multiplying the final acceptance percentage by the remaining number of shares.

Source: Financial statements

The total offer is for ~81 million shares, and after the linear distribution of 25%, approximately ~60 million shares would remain for proration. Assuming there are ~173 million total eligible shares to participate, excluding those held by the family, close associates, and treasury stock, we would have a maximum acceptance ratio of 40%.

It implies that, for the remaining 6,500 shares, if the acceptance percentage is 40%, only another 2,600 shares would be accepted in the offer through proration.

It should be noted that these numbers are based on the number of shareholders in 2017, assuming full participation of the "float." The reality is that Prosegur Cia is currently trading at lows from 2005, so many shareholders at this price might still be in losses and decide not to participate.

Regarding institutional funds, crucial for the second stage of proration, we doubt they will participate massively as analysts value Prosegur Cia between €2 and €3.50.

If the recent experience with FCC is repeated, the partial takeover bid for Prosegur Cia might not be fully completed. The FCC partial takeover bid was targeted at 7%, and ultimately, only 4.5% participated.

The Prince: Buying Prosegur Cash (CASH)

Some speculations suggest that the partial takeover bid for Prosegur Cia is part of a more significant corporate move.

Regarding the partial takeover bid to acquire 75% of Prosegur Cia, there are doubts about why drain liquidity from the stock when the family already controls around 60% of the company. Although we don't doubt that this offer is a result of the opportunity presented by Prosegur Cia's recent lows, there might be a more interesting possibility: the definitive delisting of the 20% of Prosegur Cash, a company owned about 80% by Prosegur Cia.

Prosegur Cash is the subsidiary dedicated to cash transit and management, a slow-growth business but with a leading position in some Latin American countries where banking penetration remains low.

Prosegur Cash went public through an IPO in 2017 at a price of €2, where Prosegur Cia aimed to highlight this highly profitable division. Gut Revoredo stated:

"We are convinced that [Prosegur Cash] will be one of the most important companies in the market."

Seven years later, the company is trading at €0.47, 77% below the IPO price. This is despite continuous sales growth, a topic we'll delve into in the second part of this story, left for another post.

Moving on...

Having failed in the attempt to highlight the value of Prosegur Cash, it seems sensible and would create value for Prosegur Cia to acquire Prosegur Cash's shares for less than half the IPO price.

Additionally, we believe there's a good chance that the true final intention of the partial takeover bid for Prosegur Cia is to facilitate an exchange of Prosegur Cia shares for all externally held Prosegur Cash shares, without the family losing control of the group and returning the drained liquidity to Prosegur Cia's stock.

How could the operation be orchestrated?

Source: Financial statements

Suppose the family tries to delist Prosegur Cash by paying a 35% premium (common in such operations). The exchange ratio after the partial takeover bid would be 2.88 Prosegur Cash shares for each Prosegur Cia share.

Source: Own elaboration

How many shares would Prosegur Cia have to issue to delist Prosegur Cash with a 35% premium?

Once the partial takeover bid for Prosegur Cia by Gubel is completed, the family's percentage of Prosegur Cia shares would increase to >75%.

Source: Own elaboration

Subsequently, to launch a takeover bid for Prosegur Cash with a premium, Prosegur Cia would have to issue 93,208,432 new shares.

How would the family's percentage look after the dilution?

Source: Own elaboration

Recapping:

Assuming the partial takeover bid for Prosegur Cia closes at €1.83, the family increases its stake from 62% to 77%.

Later, Prosegur Cia could launch an exclusion bid for Prosegur Cash with a 35% premium through an exchange of 2.88 Prosegur Cash shares for each Prosegur Cia share.

Prosegur Cia would issue 93 million shares, resulting in family dilution from ~77% to ~66%, still maintaining control of Prosegur Cia comfortably and even having room to raise the offer.

The family succeeds in excluding Prosegur Cash at a premium price of €0.63, 70% below the IPO placement price in 2017.

Why not directly exclude Prosegur Cash through a purchase by Prosegur Cia without the prior family partial takeover bid?

If done with shares: The family would be diluted and close to losing control.

If done with debt: The balance sheet would be compromised when debt is already at €1.05 billion. Additionally, including the possible purchase of Prosegur Cash, net debt would increase to €1.2 billion, a ratio slightly above 2.5x Net Debt / EBITDA.

Finally, what would be the valuation of Prosegur Cia and Prosegur Cash if the operation doesn't go through and we get stuck?

This is material for another entry... coming soon in the second part of this story.

Until next time!"