Societe Fonciere Lyonnaise : Pase raso al pie para Chutar (English version at the end)

“Es como un deja vu de nuevo otra vez". Yogi Berra

Nos gusta la idea de que los tipos han alcanzado el pico, y más tarde o temprano, veremos las bajadas. Desde luego, si esto es así, se pueden encontrar muchas maneras “coherentes” de jugarlo.

Según los analistas de BofA, hay dos sectores que se benefician siempre de las primeras bajadas de tipos: Tecnología e Inmobiliario.

Con respecto a la tecnología, parece que ya ha descontado este movimiento. Aquí hay poco que rascar.

Sin embargo, creemos que algunas partes del sector inmobiliario siguen bastante penalizadas. Entre otras, todavía tenemos compañías cotizando bastante por debajo de los niveles de antes del Covid y con descuentos sobre sus valores netos contables casi en máximos.

Es el caso de Societe Fonciere Lyonnaise (SFL), la Socimi francesa que cuenta con los edificios de oficinas más prestigiosos del distrito central premium de París, que ha pasado en menos de un año, de un precio de 84€ a los niveles actuales de ~68€.

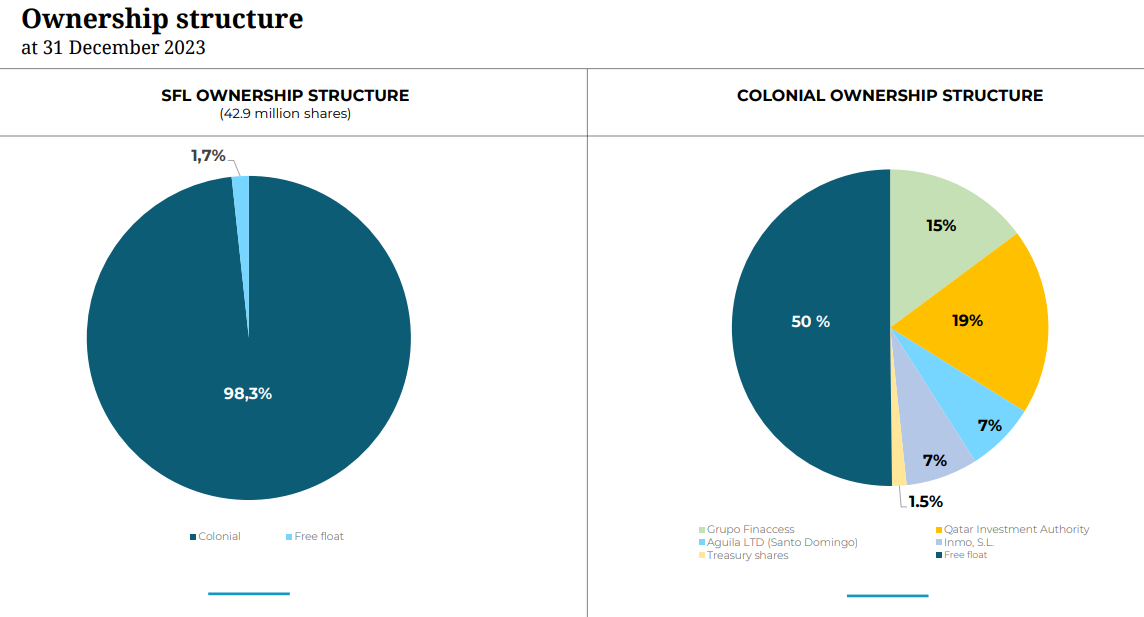

Esto podría ser irrelevante dentro del contexto del sector y en particular de oficinas si no tuviésemos en cuenta que la Socimi española Colonial es dueña del 98.3% de la compañía y que la cotización ha vuelto a los niveles en los que Colonial realizó una OPA a SFL en 2021.

Es posible que no sea nada, pero creemos que puede pasar algo aquí. Y es que a medida que se vaya asentando la situación de los tipos de interés, es bastante probable que el sector inicie la recuperación.

Nos parece que estaríamos cerca de esa recuperación, y que Colonial (en cualquier momento) podría aprovechar para lanzar la OPA de exclusión del 1.70% restante de SFL, y que debería ser por una prima no inferior al 30% con respecto al precio actual.

Breve descripción de SFL

Societe Fonciere Lyonnaise es una Socimi francesa que cuenta con uno de los mejores portafolios de oficinas en Europa, situadas principalmente en el lujoso distrito centro de París.

El valor de los inmuebles a cierre de diciembre es de €7.332m, y la situación de endeudamiento es muy moderada si tenemos en cuenta que tiene un Loan to Value (LTV) del 32.5% que, a día de hoy, estaría entre uno de los ratios más conservadores del sector. El valor neto de los activos por acción es de 87.5€ a cierre de 2023, frente a una cotización actual de 68.8€ y esto a pesar del fuerte ajuste del -18.5% en 2023 en las tasaciones contables, concretamente el Net Tangible Assets (NTA) del European Public Real Estate Association (EPRA).

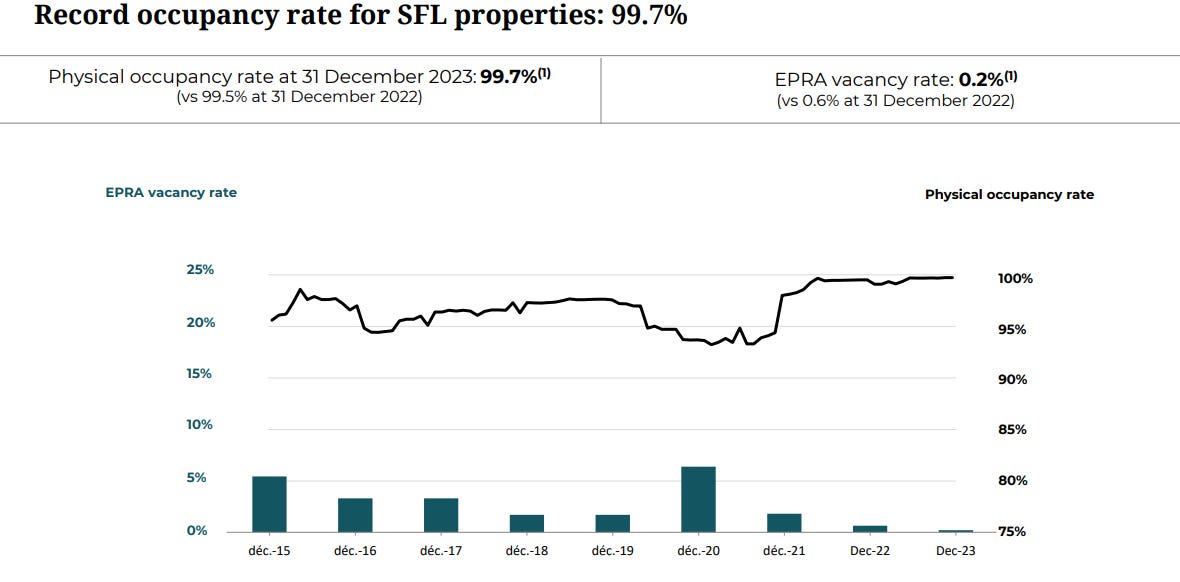

En el contexto mundial, a pesar de las noticias negativas de la situación de las oficinas en el mundo anglosajón, SFL presenta niveles récord de ocupación del 99.7%. Lo que se explica en parte por la cultura europea de oficinas, pero principalmente porque los inquilinos de SFL, son firmas de primer nivel y en una parte importante coincide donde se sitúan los headquarters.

Aumento del 82% al 98% por parte de Colonial

En junio de 2021 Colonial realizó una de las operaciones más importantes de los últimos años. La compañía compró el 13% de SFL propiedad de Predica, filial de seguros de Credit Agricole.

Con este acuerdo pasó a controlar hasta un 95% de la compañía francesa SFL desde el 82% anterior.

Además, coincidiendo con esta operación, el grupo español lanzó una OPA voluntaria por un 5% del capital adicional, que se fraguó mediante una oferta de 46€ en efectivo y cinco acciones de nueva emisión de Colonial. Esto suponía un precio total de 89€, una prima del 44% sobre los 63€ de cotización del día anterior y un descuento sobre el NTA del 43.8%.

Mientras que con ese movimiento se consiguieron hacer con el control de un 98.3%, en esta ocasión no se usó el procedimiento de venta forzosa y se decidió mantenerla cotizando en Francia.

Así lo explicó en su momento Pere Viñolas (Presidente de SFL y CEO de Colonial):

“Por el momento la operación no supondrá la desaparición de la filial ni su exclusión de la cotización en Francia”, si bien, reconoció lo siguiente: “en el medio plazo la integración total forma parte de nuestros objetivos”.

Situación actual

La compañía se encuentra cotizando en niveles de 68€, presentando una caída del ~20% con respecto a los máximos de marzo de 2023. Adicionalmente, la Socimi ha cerrado con una rentabilidad en el año 2023 de -20.6%, significativamente peor que el sector, que sube un 12.5% si miramos el índice EPRA Europe.

La mayor parte de las caídas de SFL y de las compañías con inmuebles de más calidad, estarían explicadas en su mayor parte por el movimiento de los tipos de interés, al tener portfolios con yield más ajustadas y cuyo tipo de activos por simplificar se suele comparar con las tasas libre de riesgo.

Precisamente el mínimo de la cotización de SFL se alcanzó en septiembre de 2023, en el famoso momento del “higher for longer” de Powell cuando llegó a cotizar en mínimos de 60€/acción y cuando se temía una situación de tipos altos por mucho tiempo, en un entorno de incertidumbre máxima sin apenas visibilidad en el posible techo de los tipos.

A día de hoy, aunque la situación del mercado americano invitaría a la prudencia con respecto a los datos de inflación e inicio de las bajadas de tipos, la situación de Europa es radicalmente diferente, con cierta debilidad en los datos macro.

Es de esperar que, si este movimiento de tipos se revierte, SFL sea una de las grandes beneficiadas debido a que cuenta con una cartera de inmuebles más defensivos y el posible impacto en rentas debería ser más limitado. Lo estamos viendo con la actual tasa de ocupación del ~100% de SFL y con el incremento de rentas en 2023 del 8.5%.

Pere Viñolas lo explicó bien en la conferencia de resultados de Colonial para los primeros nueve meses de 2023, cuando todavía no se había producido parte del ajuste contable en las valoraciones de los activos que hemos visto en el último trimestre en los resultados de SFL presentados el 14 de febrero de 2024:

“If we think about it, that means that as of now, we are observing the first leg of this adjustment happening, which is yield expansion happening. This may end soon, not so soon. But as we said, we've gone a long way, but it's a one off. Once this is done, this is over. And then comes the second leg, which is the fact that we pass through in our cash flows the inflation, as it's happening. So therefore it's a kind of a V shape kind of a performance, the one that should be impacting in our valuation, not also in our relation, but in the valuation of our sector. But to answer your question, as I said, we believe that, having gone a long way, this is not finished yet, and we may still see further adjustments by year end”

Pere Viñolas cree que las subidas de tipos para contener la inflación tienen dos impactos sobre el valor de las compañías inmobiliarias como SFL, que se reflejan a una velocidad distinta. Primero se produce el impacto negativo en los valores netos contables de los inmuebles, por culpa de los tipos de interés más elevados. Posteriormente, la capacidad de los inmuebles de trasladar el incremento en la inflación a las rentas resulta en un valor contable más alto. De ahí la “V shaped performance” descrita por el CEO de Colonial.

Posible OPA de exclusión

La cotización actual de 68.8€, se sitúa cerca de los niveles previos de 63€ de la OPA de 2021.

En términos de EPRA NTA, la operación se lanzó cuando este se situaba en 102€ frente a los 87.5€ publicado del último cierre de diciembre.

Si bien es posible que Colonial quisiera realizar la potencial OPA con el mismo descuento sobre el NTA que en 2021 o al menos trasladar la pérdida de valor contable al precio de adquisición (lo que implicaría un precio de unos 76€ o de 84.5€), no tenemos claro que el regulador viese con buenos ojos una OPA a un precio inferior a la del 2021. Además, aunque en estos últimos términos contables la acción parecería menos atractiva, hay que tener en cuenta que el NTA es un indicador atrasado, y que se sólo en 2023 ya se ha realizado un ajuste del 20%, muy en línea con el movimiento de la cotización. Lo que indica que ya no estaríamos en el momento más alto del ciclo y que parte del ajuste estaría ya está realizado.

En el caso de que se produjese una OPA, sería lógico asumir una prima de al menos el 30%, que rondaría los 89€ de cotización, precio al que se planteó la OPA anterior. Prima en línea con este tipo de operaciones, y donde no creemos que el regulador plantease objeciones.

Adicionalmente, encontramos que este escenario de valoración no parece desencaminado si tomamos como referencia las últimas ventas de acciones a mercado de Boulte Dimitri, CEO de SFL, en el entorno de 80€.

¿Como se podría instrumentalizar esta OPA?

Este movimiento implicaría un desembolso de ~€65m para Colonial, es decir, apenas un 2.5% de la capitalización de mercado actual y no tendría un impacto relevante en ratio de LTV. Además, Colonial ha realizado varias ventas de activos no estratégicos durante 2023 con primas sobre su NTA.

Dado que la cotización de Colonial, se encuentra en mínimos de varios años, creemos que tendría sentido por el “pequeño” importe a desembolsar, realizar una operación en cash.

Además de generar valorar por el descuento EPRA NTA de SFL, podría ser aprovechada para mandar un mensaje al mercado de ahorro de costes y de simplificación de la estructura, en un momento de presión para la acción como el actual.

Nos gustaría recordar qué pensamos sobre el coste de mantener un 1.70% de una compañía cotizada a través de una idea similar en nuestra tesis de hace unos meses de NH en https://cocoabeanspodcast.substack.com/p/nh-hoteles-y-la-guerra-de-minor-con.

Conclusión

Los niveles actuales de SFL invitan a que Colonial excluya definitivamente a la compañía a un precio mínimo de 89€, cotización de la OPA anterior y con prima mínima del 30%.

De no producirse, por querer seguir manteniendo algún tipo de vínculo con el regulador francés (aunque lo dudamos), esperamos que los vientos en contra que han llevado a la acción a situarse en un rango no visto desde la OPA de 2021, lleven ahora a la cotización a recuperar los niveles de hace unos meses del entorno de 84€.

En el hipotético caso de mantenerse presionada por iliquidez, con unos accionistas desanimados por la falta de una OPA e incluso dándose la tesitura de que el sector hiciese un re-rating, si la acción se quedase estancada, entendemos que la oportunidad para Colonial se acrecentaría. Llegado el caso, Colonial no tendría más remedio que lanzar una OPA acreditativa posiblemente con títulos de Colonial.

Mientras tanto, nos podemos sentar en una compañía con los mejores activos del sector: que cuenta con una tasa de ocupación del 100%, LTV del 32% después de un fuerte ajuste de valoración, con un dividendo del 3.4% y que ya ha tenido uno de los peores comportamientos relativos en bolsa del sector.

Recursos adicionales:

Presentación de resultados de SFL de 2023:

https://www.fonciere-lyonnaise.com/wp-content/uploads/2024/02/cp140224va.pdf

Societe Fonciere Lyonnaise: Low driven pass to hit

It's deja vu all over again. Yogi Berra.

We like the idea that interest rates have peaked, and sooner or later, we'll see declines. Certainly, if this is the case, there are many "coherent" ways to play it.

According to BofA analysts, two sectors always benefit from the initial interest rate declines: Technology and Real Estate.

Regarding technology, it seems to have already priced in this movement. There's little to gain here.

However, we believe that some parts of the real estate sector are still quite undervalued. Among others, there are still companies trading well below pre-Covid levels with discounts on their net asset values nearly at their peaks.

This is the case for Societe Fonciere Lyonnaise (SFL), the French REIT that owns the most prestigious office buildings in the premium central district of Paris. In less than a year, its price has dropped from €84 to current levels of ~€68.

This might seem irrelevant within the sector's context, particularly for offices, if we didn't consider that the Spanish REIT Colonial owns 98.3% of the company, and the stock has returned to the levels at which Colonial launched a takeover bid for SFL in 2021.

It might be nothing, but we believe something could happen here. As interest rate situations stabilize, the sector's recovery is quite probable.

It seems we might be close to that recovery, and Colonial (at any moment) could take advantage of it by launching a takeover bid for the remaining 1.70% of SFL, offering a premium of no less than 30% compared to the current price.

Brief description of SFL

Societe Fonciere Lyonnaise is a French REIT with one of the best office portfolios in Europe, mainly located in the luxurious central district of Paris.

The property value at the end of December is €7.332 million, and the debt situation is very moderate, considering it has a Loan to Value (LTV) of 32.5%, currently among the most conservative ratios in the sector. The net asset value per share is €87.5 as of the 2023 year-end, compared to the current stock price of €68.8, despite the significant -18.5% adjustment in 2023 in accounting valuations, specifically the Net Tangible Assets (NTA) of the European Public Real Estate Association (EPRA).

On a global scale, despite negative news about office situations in the Anglo-Saxon world, SFL presents record occupancy levels of 99.7%. This is partly explained by the European office culture, but mainly because SFL's tenants are top-notch firms, and a significant portion coincides with where their headquarters are located.

Source: SFL's 2023 year-end results presentation Increase from 82% to 98% by Colonial

In June 2021, Colonial executed one of the most significant operations in recent years. The company acquired the 13% of SFL owned by Predica, a subsidiary of Credit Agricole insurance.

With this agreement, Colonial increased its control to 95% of the French company, up from the previous 82%.

Additionally, coinciding with this operation, the Spanish group launched a voluntary takeover bid for an additional 5% of the capital, which was accomplished through an offer of €46 in cash and five newly issued Colonial shares. This amounted to a total price of €89, a premium of 44% over the €63 share price the day before and a discount on the NTA of 43.8%.

Source: SFL's 2023 year-end results presentation

While with that move they secured control of 98.3%, this time, they didn't use the forced sale procedure and decided to keep it listed in France.

This was explained by Pere Viñolas (Chairman of SFL and CEO of Colonial) at the time:

"For the time being, the operation will not lead to the disappearance of the subsidiary or its exclusion from trading in France," although he acknowledged the following: "in the medium term, complete integration is part of our objectives."

Current situation

The company is trading at €68, presenting a drop of around 20% from the highs of March 2023. Additionally, the REIT closed the year 2023 with a return of -20.6%, significantly worse than the sector, which is up 12.5% when looking at the EPRA Europe index.

Most of the declines in SFL and companies with higher-quality properties would be explained mostly by the movement in interest rates, given their portfolios with tighter yields, whose asset types are typically compared with risk-free rates.

Precisely, the minimum stock price of SFL was reached in September 2023, during the famous "higher for longer" moment of Powell, when it traded at a minimum of €60/share, and when there were concerns about high-interest rates for a long time, in an environment of maximum uncertainty with little visibility on the possible ceiling of rates.

Today, although the situation in the American market would call for caution regarding inflation data and the start of interest rate declines, Europe's situation is radically different, with some weakness in macro data.

It is expected that if this interest rate movement reverses, SFL would be one of the big beneficiaries because it has a portfolio of more defensive properties, and the potential impact on rents should be more limited. We are seeing this with the current occupancy rate of ~100% for SFL and the rent increase of 8.5% in 2023.

Pere Viñolas explained it well at the Colonial results conference for the first nine months of 2023 when part of the accounting adjustment in asset valuations hadn't occurred yet, as seen in SFL's results presented on February 14, 2024:

"If we think about it, that means that as of now, we are observing the first leg of this adjustment happening, which is yield expansion happening. This may end soon, not so soon. But as we said, we've gone a long way, but it's a one-off. Once this is done, this is over. And then comes the second leg, which is the fact that we pass through in our cash flows the inflation, as it's happening. So therefore it's a kind of a V-shape kind of a performance, the one that should be impacting in our valuation, not also in our relation, but in the valuation of our sector. But to answer your question, as I said, we believe that, having gone a long way, this is not finished yet, and we may still see further adjustments by year end."

Pere Viñolas believes that interest rate hikes to contain inflation have two impacts on the value of real estate companies like SFL, which are reflected at a different pace. First, there's the negative impact on the accounting net values of the properties, due to higher interest rates. Subsequently, the ability of the properties to pass on the inflation increase to rents results in a higher accounting value. Hence the "V-shaped performance" described by Colonial's CEO.

A possible squeeze out

The current stock price of €68.8 is close to the previous levels of €63 from the 2021 takeover bid.

In terms of EPRA NTA, the operation was launched when it was at €102 compared to the €87.5 published at the latest December closing.

While it's possible that Colonial would want to carry out the potential takeover bid with the same discount on the NTA as in 2021 or at least transfer the loss of accounting value to the acquisition price (which would imply a price of about €76 or €84.5), we're not clear if the regulator would view favorably a takeover bid at a price lower than that of 2021. Additionally, even though in these latest accounting terms, the stock might seem less attractive, it should be considered that NTA is a lagging indicator, and the 20% adjustment has already been done in 2023, very much in line with the stock's movement. This indicates that we are no longer at the peak of the cycle, and part of the adjustment has already taken place.

In the event of a takeover bid, it would be reasonable to assume a premium of at least 30%, reaching around €89, the price at which the previous takeover bid was proposed. This premium aligns with these types of operations, and we don't believe the regulator would raise objections.

Additionally, we find that this valuation scenario doesn't seem off course if we take as a reference the latest market share sales by Boulte Dimitri, CEO of SFL, at around €80.

How could this takeover bid be implemented?

This move would imply an outlay of ~€65 million for Colonial, barely 2.5% of the current market capitalization and would not have a relevant impact on the LTV ratio. Furthermore, Colonial has carried out several sales of non-strategic assets during 2023 with premiums on its NTA.

Given that Colonial's stock price is at multi-year lows, we believe it would make sense, given the "small" amount to be disbursed, to carry out a cash operation.

In addition to generating value due to the EPRA NTA discount of SFL, it could be leveraged to send a message to the market about cost savings and simplification of the structure, at a time of pressure for the stock as it currently stands.

We would like to remind you what we think about the cost of maintaining a 1.70% stake in a listed company through a similar idea in our thesis from a few months ago about NH in https://cocoabeanspodcast.substack.com/p/nh-hoteles-y-la-guerra-de-minor-con.

Conclusion

The current levels of SFL invite Colonial to definitively exclude the company at a minimum price of €89, the price of the previous takeover bid and with a minimum premium of 30%.

If it doesn't happen, perhaps due to wanting to continue maintaining some kind of link with the French regulator (although we doubt it), we expect that the headwinds that have led the stock to a range not seen since the 2021 takeover bid will now drive the stock to recover the levels of a few months ago, around €84.

In the hypothetical case of remaining under pressure due to illiquidity, with shareholders discouraged by the lack of a takeover bid, and even in the scenario where the sector undergoes a re-rating, if the stock were to stay stagnant, we understand that the opportunity for Colonial would increase. In that case, Colonial would have no choice but to launch a confirmatory takeover bid, possibly with Colonial shares.

Meanwhile, we can sit in a company with the best assets in the sector: with a 100% occupancy rate, LTV of 32% after a significant valuation adjustment, a 3.4% dividend, and has already had one of the worst relative stock performances in the sector.

| Una publicación invitada por

|