Liberty Global: Parte IV - No puedes ser el más grande pero si el mas inteligente (English versión at the end)

¡Salta la sorpresa en las gaunas!

“Siempre hay un tesoro oculto en la nevera, solo tienes que buscarlo”. Homer Simpson.

¡Que buen amigo tenemos en Telefónica!. Es posible que esto fuese lo que inmediatamente pensó John Malone (dueño de Liberty), al ver la noticia que Bloomberg publicó en la tarde del miércoles.

https://www.bloomberg.com/news/articles/2025-05-14/telefonica-is-said-to-draw-up-plans-for-liberty-s-stake-in-vmo2?srnd=homepage-europe

Telefónica tendría planes o estaría analizando tomar el control de Virgin Media O2. Esta noticia, aparte de ser bastante inesperada, es muy muy trascendente para los accionistas de Liberty.

Brevemente, para el que no siga esta historia, Virgin Media O2 es una Joint Venture 50/50 que surgió de la fusión en 2021 de O2, propiedad de Telefónica, y de Virgin Media, propiedad de Liberty. El principal racional era competir con BT, y unir fuerzas, por un lado Virgin, con fuerte presencia en red fija y televisión por cable y por el otro, 02 una de las principales operadoras de red móvil de UK.

Como contamos en la entrada anterior sobre Liberty:

El principal catalizador para Liberty en 2025, iba a ser la creación y posible monetización de una Netco, a partir de la red fija de Virgin Media. Sin embargo, hace apenas unos días, en la conferencia de resultados de Liberty, se notificó al mercado la pausa del proyecto a petición de Telefónica.

https://www.datacenterdynamics.com/en/news/virgin-media-o2-pauses-netco-stake-sale-in-uk-as-telef%C3%B3nica-review-continues/

El motivo para la paralización de la Netco, era que tras el cambio de presidencia y management en Telefónica, se estaría haciendo una revisión estratégica de toda la compañía. Principalmente, la intención del nuevo ejecutivo, es simplificar la compañía vendiendo activos non core de su época “imperialista”, (recientemente han vendido los activos de Argentina o Perú) y centrarse en consolidar su posicionamiento en Europa.

El tema del retraso de la Netco, no nos preocupaba en inicio, ya que la operación tiene bastante sentido sobre todo para Telefónica, principalmente por la reducción de la deuda, pero lo que no podíamos imaginar, es que está revisión podría derivar en la compra de la participación de Virgin Media restante.

¿Qué implicaciones tendría esto para Liberty?

Por simplificar, prácticamente pasar de mendigo, a príncipe. Veamos porqué.

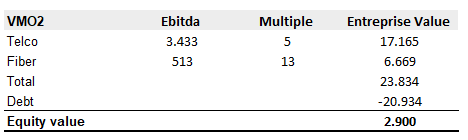

Esta es nuestra última valoración de Liberty por Suma de partes.

Fuente: Elaboración propia

Como se puede comprobar, el stake de Virgin Media O2 está valorado en ~5$ por acción, lo que ya de por sí es interesante, cuando estás cotizando en el entorno de 9,70$.

Yendo a mínimos, implica que si vendiesen su parte de Virgin por 5$, solo el cash total del holding, equivaldría a la capitalización de mercado actual. Demasiado bueno para un grupo de ejecutivos que ha recomprado el 60% sus acciones en 7 años.

Además, en está ocasión nuestro precio es tremendamente conservador. Está calculado separando la red para estimar el valor de una posible Netco, y una valoración para la parte restante o ServCo, con un múltiplo de 5x EV/EBITDA, uno de los múltiplo más bajos de todo el mercado de telecomunicaciones en Europa.

Source: Elaboración propia. Valoración del 100% de VMO2 en libras. Explicado en detalle en: Liberty Global: Parte III- No puedes ser el más grande, pero sí el más inteligente

Source: Elaboración propia

Pero…amigo mío!, estamos hablando de una transacción, y con una prima de control, lo que encarece bastante más la operación. Primero porque en el “mundo real”, las operaciones a menudo se hacen con un sentido estratégico, y permiten llevar a las compañías a pagar más, como única opción de consolidar cuota en un mercado específico. Y segundo, porque los múltiplos del mercado cotizado, a menudo recogen valoraciones penalizadas por el contexto actual, o modas dentro del mundo de la inversión financiera, alejado de la realidad del sector.

El ejemplo más pertinente, sería el múltiplo al que se materializó la fusión entre Virgin Media y 02 en 2021.

La entidad combinada se valoró en £31.4bn: y la valoración implícita del canje fue de 7.5x Ebitda de O2 y de algo más de 9x el Ebitda de Virgin media propiedad de Liberty en ese momento.

Otros ejemplos recientes en transacciones, podrían ser:

La Opa de exclusión a Másmovil en 2020 por parte de Lorca (KKR, Cinven y Providence) a un múltiplo de 8.5x EV/EBITDA

La Opa de Euskaltel por parte de Másmóvil que implicaba un EV/EBITDA21 de 10.1x.

Y la fusión entre Masmóvil y Orange con un múltiplo ajustado de Ebitda alrededor de 7.2x Ebitda para Orange y 8.7x Ebitda para Másmóvil.

En el caso de Virgin Media, el endeudamiento de la compañía es relativamente alto (+5x DN/EBTIDA) lo que hace que cualquier variación del múltiplo final sea bastante significativa.

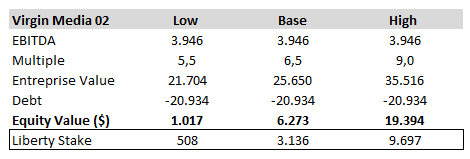

Veamos el siguiente análisis de sensibilidad de la valoración de Virgin:

Source: elaboración propia

Oh Jesús!, en el escenario base (múltiplo de solo 6.5x), la valoración de Virgin media equivale aproximadamente a toda la capitalización de mercado de Liberty.

Lo dicho, de mendigo a príncipe.

- Filmaffinity")

¿Qué esperar de esta noticia?

El posible interés de Telefónica por el stake de Liberty no ha sido confirmado, pero tampoco ha sido desmentido. Es posible que de momento sea solo una de las opciones que tengan sobre la mesa con la nueva estrategia de consolidar en ciertos países.

Algunas voces del mercado, le darían veracidad pero sería una operación, que de tener luz verde, no se anunciaría hasta el Capital Market Day previsto para el segundo semestre de este año.

Aunque el principal escollo sería el endeudamiento actual de Telefónica y la foto final en el caso de adquirir un participación de control, que implicaría una consolidación de los más de £20bn de endeudamiento, y que ahora, al ser un JV, estarían por puesta en equivalencia.

La foto de Telefónica actual es la siguiente:

Telefónica tiene actualmente una deuda de 2.7x DN/EBITDAal, si tomase el control y consolidase el 100% de la deuda de Virgin Media, la deuda de Telefónica pasaría a ser +€50bn contando con el importe de la adquisición. El ratio DN/EBITDAal se dispararía a casi 4x.

Sería necesario un plan de desinversión por parte de Telefónica que contase con la monetización de las Netco pendientes, tanto en España con Zegona, como la Netco paralizada en UK, otros activos Non Core y no sería descartable una ampliación de capital.

Conclusión

Esta tesis va de esto, poner en valor las participaciones del holding, que el mercado no está valorando. Ya lo hemos visto con el Spin off de Sunrise, donde el descuento holding se redujo y nuestro trade llegó a suponer una rentabilidad del 40%.

Un operación que valore Virgin Media a los precios sugeridos en una transacción con prima de control, ya sea por el 100% de la participación, o por una parte, y a los precios actuales, supondría un importante catalizador para ir cerrando el descuento holding. Mucho más importante que el que se dió en la operación de Sunrise en Diciembre de 2024.

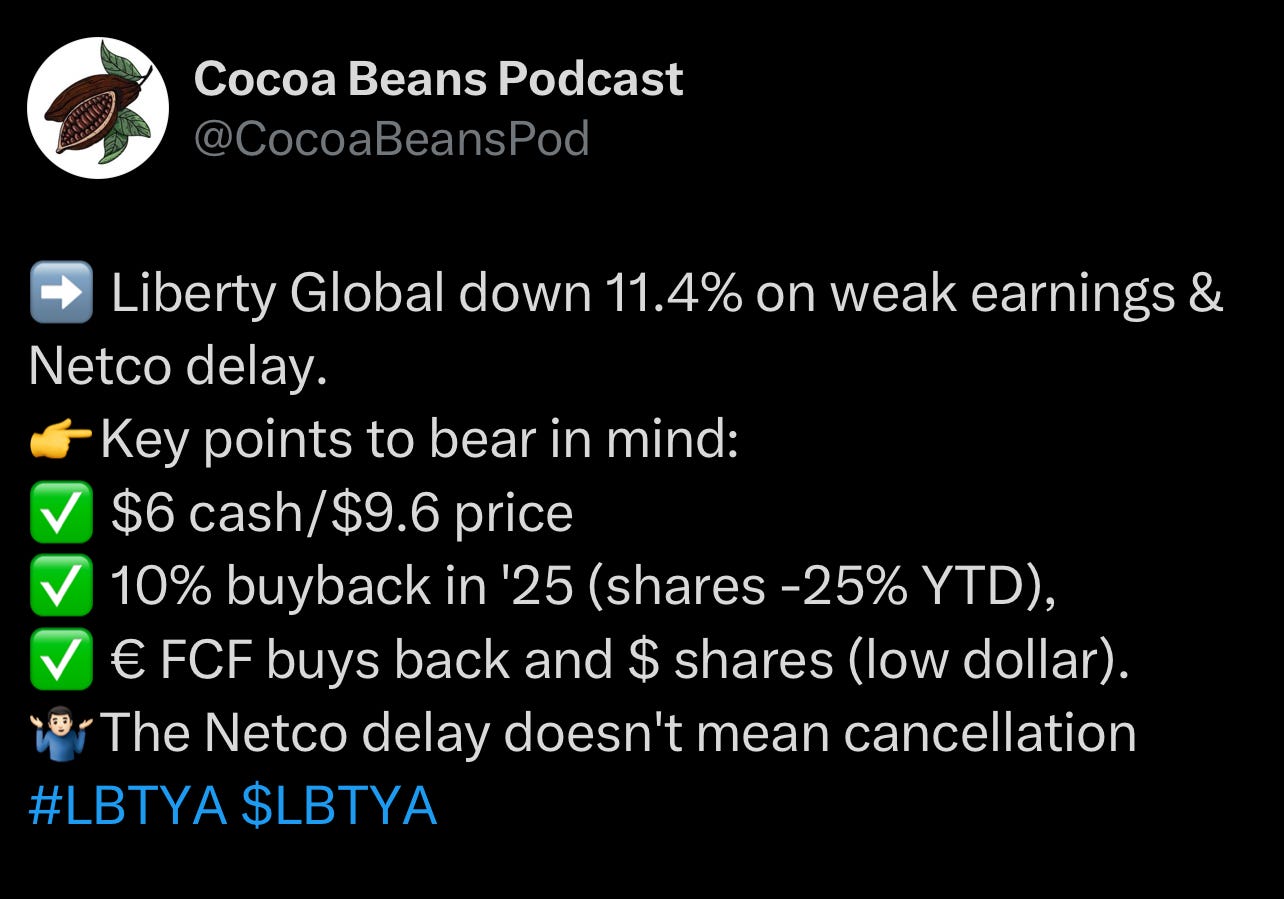

El otro día lanzábamos el siguiente tweet en nuestra cuenta CocoaBeansPod en Twitter a consecuencia de los resultados, día que Liberty llegó a corregir hasta un 11% y pasó de niveles de 11$ a 9$.

Totalmente alineados con este mensaje, está sería nuestra carta a los reyes magos:

Que el mercado no le de credibilidad a esta noticia y que se mantenga cotizando a estos niveles o incluso por debajo.

Que el management ejecute su plan para 2025 de recomprar hasta un 10% de las acciones en circulación.

Y que después de retirar tal cantidad de acciones a estos precios, Telefónica acometa está adquisición.

Si tuviésemos esta gran fortuna, nos resultaría raro que esto no fuese un bagger.

Atentamente,

Cocoa beans podcast

Liberty Global: Part IV - You Can't Be the Biggest, but You Can Be the Smartest

"There's always a hidden treasure in the fridge, you just have to look for it." - Homer Simpson.

What a good friend we have in Telefónica!. This might have been what John Malone (owner of Liberty) immediately thought upon seeing the news that Bloomberg published on Wednesday afternoon.

https://www.bloomberg.com/news/articles/2025-05-14/telefonica-is-said-to-draw-up-plans-for-liberty-s-stake-in-vmo2?srnd=homepage-europe

Telefónica might be planning or considering taking control of Virgin Media O2. This news, aside from being quite unexpected, is very significant for Liberty's shareholders.

Briefly, for those who haven't been following this story, Virgin Media O2 is a 50/50 joint venture that emerged from the 2021 merger of O2, owned by Telefónica, and Virgin Media, owned by Liberty. The main rationale was to compete with BT and to join forces, with Virgin having a strong presence in fixed network and cable television, and O2 being one of the main mobile network operators in the UK.

As we mentioned in the previous entry about Liberty:

The main catalyst for Liberty in 2025 was going to be the creation and possible monetization of a Netco, based on Virgin Media's fixed network. However, just a few days ago, during Liberty's earnings conference, the market was notified of the project's pause at Telefónica's request.

https://www.datacenterdynamics.com/en/news/virgin-media-o2-pauses-netco-stake-sale-in-uk-as-telef%C3%B3nica-review-continues/

The reason for the Netco's halt was that, following the change in presidency and management at Telefónica, a strategic review of the entire company is being conducted. Primarily, the new executive's intention is to simplify the company by selling non-core assets from its 'imperialist' era (recently, they have sold assets in Argentina and Peru) and focus on consolidating its position in Europe.

Initially, the delay of the Netco did not concern us, as the operation makes a lot of sense, especially for Telefónica, mainly due to debt reduction. However, what we could not imagine is that this review could lead to the purchase of the remaining Virgin Media stake.

What implications would this have for Liberty?

To simplify, it would practically mean going from beggar to prince. Let's see why.

This is our latest valuation of Liberty by Sum of the Parts.

Source: Own elaboration

As can be seen, the stake in Virgin Media O2 is valued at approximately $5 per share, which is already interesting when you are trading around $9.70.

At a minimum, it implies that if they sold their part of Virgin for $5, the total cash of the holding would equal the current market capitalization. Too good for a group of executives who have repurchased 60% of their shares in 7 years.

Additionally, on this occasion, our price is extremely conservative. It is calculated by separating the network to estimate the value of a possible Netco, and a valuation for the remaining part or ServCo, with a multiple of 5x EV/EBITDA, one of the lowest multiples in the entire telecommunications market in Europe.

Source: Own elaboration. Valuation of 100% of VMO2 in pounds. Explained in detail in: Liberty Global: Part III - You can't be the biggest, but you can be the smartest.

Source: Own elaboration

But... my friend! We are talking about a transaction, and with a control premium, which makes the operation considerably more expensive. First, because in the 'real world,' transactions are often done with a strategic sense, allowing companies to pay more as the only option to consolidate market share in a specific market. Second, because the multiples of listed markets often reflect valuations penalized by the current context or trends within the financial investment world, far from the sector's reality.

The most pertinent example would be the multiple at which the merger between Virgin Media and O2 materialized in 2021.

The combined entity was valued at £31.4bn: and the implicit valuation of the exchange was 7.5x EBITDA for O2 and slightly more than 9x EBITDA for Virgin Media owned by Liberty at that time.

Other recent transaction examples could be:

The takeover bid for MásMóvil in 2020 by Lorca (KKR, Cinven, and Providence) at a multiple of 8.5x EV/EBITDA.

The takeover bid for Euskaltel by MásMóvil, which implied an EV/EBITDA21 of 10.1x.

The merger between MásMóvil and Orange with an adjusted EBITDA multiple of around 7.2x EBITDA for Orange and 8.7x EBITDA for MásMóvil.

In the case of Virgin Media, the company's indebtedness is relatively high (+5x Net Debt/EBITDA), which makes any variation in the final multiple quite significant.

Let's look at the following sensitivity analysis of Virgin's valuation:

Source: Own elaboration

Oh Jesus! In the base scenario (with a multiple of just 6.5x), the valuation of Virgin Media is approximately equivalent to the entire market capitalization of Liberty.

As I said, from beggar to prince.

What to expect from this news?

The possible interest of Telefónica in Liberty's stake has not been confirmed, but it has not been denied either. It is possible that, for now, it is just one of the options they have on the table with the new strategy of consolidating in certain countries.

Some market voices would give it credibility, but it would be an operation that, if given the green light, would not be announced until the Capital Market Day scheduled for the second half of this year.

Although the main obstacle would be Telefónica's current indebtedness and the final picture in the case of acquiring a controlling stake, which would imply a consolidation of the more than £20bn of debt, and which now, being a JV, are accounted for by the equity method.

The current picture of Telefónica is as follows:

Telefónica currently has a debt of 2.7x Net Debt/EBITDA. If it took control and consolidated 100% of Virgin Media's debt, Telefónica's debt would exceed €50bn, including the acquisition amount. The Net Debt/EBITDA ratio would soar to nearly 4x.

A divestment plan by Telefónica would be necessary, including the monetization of pending Netcos, both in Spain with Zegona and the halted Netco in the UK, and a capital increase would not be ruled out.

Conclusion

This thesis is about valuing holding stakes that the market is not valuing. We have already seen this with the Sunrise spin-off, where the holding discount was reduced and the trade yielded a 40% return.

An operation that values Virgin Media at the suggested transaction prices with a control premium, whether for 100% of the stake or a part, and at current prices, would be a significant catalyst to close the holding discount. Much more important than the Sunrise operation in December 2024.

The other day we posted the following tweet on our CocoaBeansPod Twitter account as a result of the earnings, a day when Liberty corrected up to 11% and dropped from $11 to $9.

Totally aligned with this message, this would be our letter to Santa Claus:

That the market does not give credibility to this news and that it remains trading at these levels or even below.

That management executes its plan for 2025 to repurchase up to 10% of the outstanding shares.

And that after retiring such a quantity of shares at these prices, Telefónica undertakes this acquisition.

If we had this great fortune, it would be strange if this did not become a bagger.

Sincerely,

Cocoa beans podcast

DISCLAIMER

The information contained in this website and associated podcast is not, and should not be construed as, investment advice, and does not purport to be, or express any opinion concerning the price at which the securities of any company may trade at any time.

Each investor should make their own decisions regarding the prospects of any security or financial instrument discussed herein based on their own review of publicly available information and should not rely on the information contained herein.

The information contained in this website has been prepared based upon publicly available information and independent research. The authors do not guarantee the accuracy or completeness of the information provided. All statements and expressions herein are solely the opinion of the authors and are subject to change without notice.

Any projections, market outlooks or estimates mentioned herein are forward-looking statements and are based on certain assumptions and should not be construed as indicative of actual events that will occur. Other events not taken into account may occur and may significantly affect the performance or returns of the securities discussed herein. Except as otherwise indicated, the information provided herein is based on matters as they exist at the date of preparation and not as at any future date, and the authors assume no obligation to correct, update or revise the information in this document or to provide any additional materials.

The opinions, thoughts and viewpoints expressed in this blog and associated podcast are solely those of its authors, and do not necessarily reflect the opinions, thoughts or viewpoints of any of their past, present or future employers, or any other organization, committee or other group or individuals with whom they may be associated.

The authors, the authors’ affiliates and clients of the authors’ affiliates may currently have long or short positions in the securities of some of the companies mentioned herein, or may take such positions in the future (and may therefore benefit from fluctuations in the trading price of the securities). To the extent that such persons have such positions, there is no guarantee that such persons will maintain such positions.

Neither the authors nor any of their affiliates accept any liability whatsoever for any direct or consequential loss arising, directly or indirectly, from any use of the information contained herein. Moreover, nothing presented herein shall constitute an offer to sell or the solicitation of an offer to buy any securities.

Gran trabajo! Quizás uno de los activos no estratégicos que vendan sea la participación en Lionsgate. Ahora que se ha completado la spinoff entre Starz y Lionsgate puede que una plataforma de streaming o estudio lance una OPA.