Phinia Inc (English version at the end)

Una empresa aburrida en una industria impopular que podría devolver el 100% de su capitalización de mercado a los inversores en unos pocos años.

David Einhorn, presidente de Greenlight Capital, lleva repitiendo el mismo punto en casi todas las entrevistas que ha dado en los últimos años. En respuesta a cómo ha cambiado la industria de gestión de activos durante la última década, en la que el crecimiento de las estrategias pasivas ha echado del mercado a casi todos los inversores que tenían en cuenta la valoración en su proceso de inversión, Greenlight Capital ya no espera que el mercado reconozca o reevalúe las empresas subvaloradas en las que ellos invierten. En cambio, Greenlight se concentra mucho más en lo que las empresas mismas pueden pagar a Greenlight. David ha llegado a la conclusión de que con algunas de estas acciones, nadie va a prestar atención. Nadie nadie está haciendo el trabajo, a nadie le importa lo que la empresa dice. Simplemente no hay nadie escuchando. En consecuencia, en Greenlight Capital han reconstruido su cartera de inversiones de manera que, al menos en teoría, puedan obtener un retorno sobre su inversión basándose únicamente en lo que las empresas son capaces de pagarles en lugar de depender de otros inversores . En un reciente podcast de Colossus, David dijo:

“We used to be able to buy things and say, "Well, this is an okay company and it's at 11x earnings, but I think that the earnings are going to be 10% more over a year or two or maybe 20% more, and it will get re-rated then to 15x earnings because people will see that it's better than they thought, so the stock will go up 60% to 80% over a couple of years, then it will be fully appreciated and we'll move on to the next thing."

The problem now is if you buy that thing, even if it plays out the way it does, if it started at 11x, earnings in two years, it's very likely, instead of being at 15x earnings, feels like it's going to be at 7x earnings. We're basically at the same price with earnings up 40% over a couple of years. And you're not really going to make any money because there's nobody who is appreciating what is going on and analyzing it. It just gets lumped into a bucket.

So we need to have that story combined with, well, instead of paying 11x earnings, we're going to pay 4x earnings. And we're going to pay 4x earnings, and there's going to be a 20% buyback going on. And I think if we're able to do that. And we can do that because there's really nobody paying attention, so there are plenty of companies that are actually that cheap.

Like, you say, "Well, where do you find companies are that cheap?" There actually are companies that are that cheap in unpopular areas that don't even necessarily have bad businesses. And I think we're going to earn our returns off of buying things at much, much lower values and holding them until the capital has been fully returned.”

La idea que presentamos hoy podría ser un caso similar.

Introducción y tesis de inversión

El 6 de diciembre de 2022, BorgWarner (NYSE: BWA; capitalización de mercado de USD 7.8 billones) anunció planes para hacer un spin-off del 100% de las acciones de su negocio de Sistemas de Combustible (Fuel Systems) y Posventa (Aftermarket) bajo el nombre corporativo PHINIA Inc. (NYSE: PHIN; capitalización de mercado de USD 1.2 billones).

A través de esta transacción, BorgWarner pretende avanzar en su objetivo de convertirse en uno de los líderes del mercado en tecnología de propulsión para vehículos eléctricos, y PHINIA podrá centrarse en su negocio principal de fabricación de sistemas de combustible y venta de piezas de aftermarket.

En palabras sencillas: BorgWarner espera que el mercado les valore con un mayor múltiplo al deshacerse de la “pesada” exposición de PHINIA a los motores de combustión interna, tan odiados por el mercado.

La verdad es que como empresas separadas, ambos negocios se beneficiarán de un enfoque estratégico más concentrado y de la flexibilidad para perseguir sus diferenciadas oportunidades de mercado.

Como suele ocurrir en los spin-offs, los accionistas de BorgWarner que han recibido acciones de PHINIA han optado por vender inmediata e indiscriminadamente sus acciones de PHINIA en el mercado público, mandando el precio de la acción a un mínimo de $26.27 desde el precio de debut en el mercado de $37. Tener acciones de una empresa más pequeña y expuesta a los motores de combustión interna simplemente no encaja en los objetivos de inversión de muchos accionistas de BorgWarner, incluyendo muchos fondos indexados.

Discrepamos con la narrativa general sobre la inminente desaparición de los motores de combustión interna y creemos que el actual valor de empresa de solo 3.5 veces el EBITDA de los últimos doce meses es injustificadamente bajo.

Resumen del negocio

PHINIA es un fabricante de sistemas de combustible y un distribuidor de piezas de aftermarket. La cartera de productos de PHINIA incluye arrancadores eléctricos y alternadores para motores, contenedores que capturan los vapores de combustible antes de que escapen a la atmósfera, así como inyectores, bombas y módulos de entrega para diésel, gasolina y combustibles alternativos como hidrógeno, etanol y gas natural.

Los sistemas de combustible y soluciones de aftermarket de PHINIA permiten que los motores de combustión interna operen con máximo rendimiento, optimizando así el desempeño, aumentando la eficiencia y reduciendo emisiones.

Los productos de PHINIA se utilizan en vehículos comerciales y aplicaciones industriales (camiones de medio y gran tonelaje, autobuses y otras construcciones fuera de carretera, aplicaciones marinas, agrícolas e industriales) y vehículos ligeros (automóviles de pasajeros, camiones, furgonetas y vehículos deportivos utilitarios).

PHINIA cree que el segmento de aftermarket (~38% de las ventas totales de 2022) proporciona una base de ingresos recurrente y estable, ya que la sustitución de muchos de estos productos no es discrecional por naturaleza (si se te rompe el sistema de arranque, es muy difícil que pospongas la reparación). Además, creen (y estamos de acuerdo) que el creciente número de vehículos en la carretera, junto con la mayor edad promedio de los vehículos y el aumento de millas recorridas, llevará a una creciente demanda de sus productos de posventa.

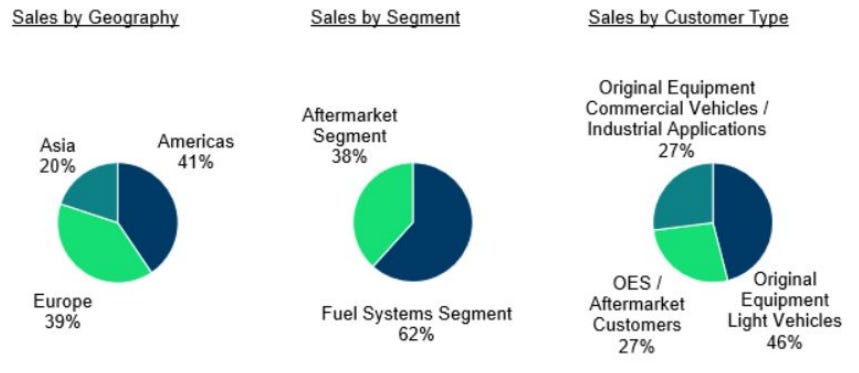

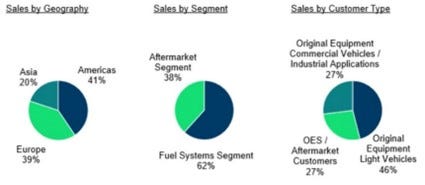

En 2022, PHINIA obtuvo el 39% de sus ingresos de Europa, el 41% de América y el 20% de Asia. Además, el 27% de sus ventas netas en 2022 fueron a fabricantes de vehículos comerciales y aplicaciones industriales, el 46% fueron a fabricantes de vehículos ligeros y el 27% a clientes de servicios y aftermarket. En 2022, General Motors representó el 12% de las ventas netas, sin ningún otro cliente que representara más del 10%. Sus cinco principales clientes representaron un total de aproximadamente el 32% de las ventas netas.

Desglose de las Ventas de 2022 por Geografía, Segmento y Tipo de Cliente:

Fuente: PHINIA

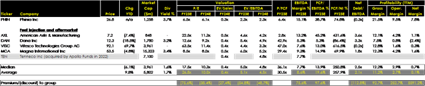

El segmento de Aftermarket genera un margen más alto que el segmento de Fuel Systems. La siguiente tabla presenta las Ventas Netas y el Resultado Operativo Ajustado por segmento:

Fuente: PHINIA

Análisis financiero

PHINIA presentó los resultados del segundo trimestre el 7 de agosto de 2023 y presentará los resultados del tercer trimestre el lunes 6 de noviembre de 2023.

Para el segundo trimestre, PHINIA logró un crecimiento en las ventas del 11.4% sobre el año anterior, hasta $887 millones. Este crecimiento fue superior al que esperamos en adelante ya que incluyó incrementos de precios a sus clientes resultante de negociaciones comerciales no contractuales para recuperar el impacto en coste de inflación en materiales sufrida el año anterior. En adelante, esperamos una tasa de crecimiento del 1-2% anual. Definitivamente no es un negocio de alto crecimiento.

La compañía también presentó un resultado operativo (EBIT) de $56 millones y un EBIT ajustado1 de $94 millones, lo que resultó en un margen operativo del 6.3% y un margen operativo ajustado del 10.6%, una mejora de 10 pb y 180 pb respecto al año anterior, respectivamente. Los márgenes también se beneficiaron de la recuperación del impacto inflacionario con efecto retroactivo al principio del año. Los costes corporativos también fueron menores en el segundo trimestre en comparación con el año anterior.

El beneficio neto presentado para el segundo trimestre ascendió a $35 millones con un margen neto del 3.9% y un EBITDA ajustado de $130 millones con un margen de EBITDA ajustado del 14.7%, una mejora de 140 pb respecto al año anterior.

En la presentación de agosto, la compañía reafirmó sus previsiones para el año completo (2023), esperando ventas de entre $3.45 billones a $3.55 billones, un EBITDA ajustado para todo el año de $485 millones a $505 millones, y márgenes de EBITDA ajustados del 13.8% al 14.3%.

También en agosto, PHINIA anunció que su Junta Directiva había aprobado un dividendo trimestral en efectivo de $0.25 por acción ordinaria (un rendimiento por dividendo de aproximadamente el 3.8% del precio actual de la acción). Además, la Junta Directiva autorizó un programa de recompra de acciones por $150 millones (aproximadamente el 12% de la capitalización de mercado de la compañía).

Brady Ericson, Presidente y CEO de PHINA, comentó:

“We are pleased to initiate a competitive quarterly dividend and a share repurchase program as we are confident in our business’s strong earnings and cash generation ability. We believe that our dividend, combined with opportunistic share repurchases, are the logical next steps in enhancing shareholder value. We remain committed to returning a substantial portion of free cash flow to shareholders, maintaining our strong balance sheet, making prudent organic investments, and selectively investing in rapidly accretive and high ROIC acquisitions. Our investments in the business will support our objective of sustainable profitable growth.”

Algo que siempre nos gusta ver en nuestras inversiones es la alineación de los intereses del equipo directivo con los de los inversores minoritarios. Según la política de compensación de BorgWarner, la cual PHINIA espera mantener en el futuro, se esperaba que los ejecutivos tengan un interés significativo en la compañía mediante acciones. Para el CEO, se espera que tenga una posición en acciones de 6 veces el valor de su salario base anual. A 22 de septiembre de 2023, Brady Ericson, Presidente y CEO, poseía 401,837 acciones con un valor total de mercado de USD 10.8 millones (aproximadamente 12.4 veces su salario base).

Sabemos que ha comprado al menos 13,194 de estas acciones a un precio promedio de $29.11 en el mercado abierto (en agosto), por un valor total de $384.077. Más allá de estas compras, sospechamos que la mayoría de sus acciones restantes le fueron otorgadas como parte de su compensación, en lugar de haberlas comprado él mismo con dinero de su propio bolsillo. Aunque sería mejor ver al CEO de la empresa comprar acciones con su riqueza personal, su actual participación en PHINIA representa una cantidad significativa en relación con su salario base, alineando sus intereses con los de los demás accionistas. De hecho, es el accionista individual más grande y el 11º inversor más grande en general.

Además, en la más reciente conferencia telefónica con analistas, mencionó que van a restablecer las métricas clave del plan de incentivos a largo plazo de la compañía, que se centrará en el valor económico y el ROIC, así como en la generación de efectivo global del negocio. Creemos que este es un buen objetivo y esperamos ver los detalles del plan.

Análisis de mercado y valoración

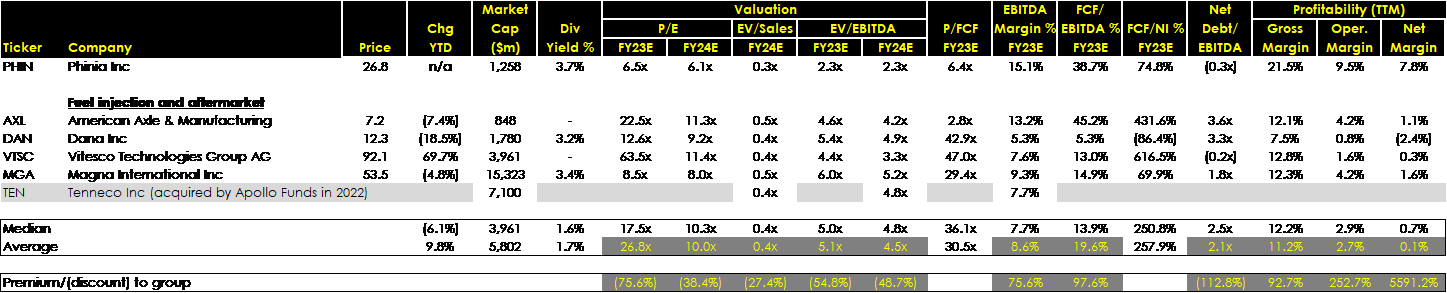

Los competidores American Axle & Manufacturing, Dana, Magna, Vitesco Technologies (que recientemente ha recibido una oferta de adquisición por parte de Schaeffler con un prima de aproximadamente el 25% en comparación con la fecha del anuncio) y Tenneco, cotizan a un múltiplo de 5.0x EV/EBITDA, en comparación con el 3.5x de PHINIA, a pesar de tener un margen de EBITDA significativamente más alto, una mejor conversión de flujo de caja y menor apalancamiento.

Fuente: elaboración propia.

Simplemente aplicando este conservador múltiplo EV/EBITDA implicaría un incremento del 60% en el precio actual de la acción, sin siquiera contar el retorno de capital adicional del 15% proveniente de dividendos y recompras de acciones. Cualquier incremento adicional de 0.1x en el múltiplo añadiría aproximadamente un 4% adicional de incremento en el precio de la acción.

Riesgos y desafíos

PHINIA es una compañía más pequeña en comparación con BorgWarner, lo que podría resultar en un aumento de los costos debido a una disminución en su poder de compra. Además, podría hacer más difícil mantener las relaciones existentes con los clientes actuales y ganar nuevos clientes. Cuando le preguntaron sobre esto en la presentación de los resultados del segundo trimestre, el CEO Brady Ericson respondió:

“I think in general the way that things were set up under the prior ownership is most of our business units were pretty stand-alone. From finance, supply chain, engineering; our plants were pretty stand-alone. So from that perspective, there's not a lot different. There's obviously going to be some differences and the fact that legal, investor relations, treasury, tax are going to be some of the additional corporate costs that we need to add to our organization because that was some of the primary support that we had from our prior parent. So from our perspective that's going to be the biggest dissynergy.

With that said, I think we're going to be a lot more nimble in supporting our business and so I think we're going to be a lot more focused on our customers and our markets to help grow our business. And that's where I made the comment earlier around our customers are actually excited about the spin because they know they're going to have a trusted partner to supply them with combustion technology; whether it's carbon neutral, carbon-free, aftermarket parts for decades and decades. And so they were quite supportive and excited about the opportunity because they see us continuing to invest in that space and we're going to continue to help them transition to carbon-free fuels going forward.”

Es decir, ser más pequeños tiene algunos aspectos negativos, pero también algunos positivos.

Otro riesgo es que esta es una compañía expuesta a los motores de combustión interna. Además del riesgo de que la transición a los vehículos eléctricos ocurra más rápido de lo esperado (una visión que no compartimos – recomendamos leer los comentarios de PeachPit y de Conor Maguire que incluimos al final de esta entrada), está el hecho de que los inversores no quieren “tocar ni con un palo” nada relacionado con motores de combustión interna. Si bien esto puede resultar en presión de venta a corto plazo, y por lo tanto una oportunidad de compra para el inversor paciente, también puede llevar a un descuento permanente si el mercado se niega a valorar este negocio correctamente. Creemos que la actitud de la compañía hacia ofrecer de retornos de capital a los accionistas mediante dividendos y recompras mitiga este riesgo.

También creemos que el múltiplo actual es excesivamente conservador dados los múltiplos históricos de los comparables, y creemos que existe el potencial de que esta compañía sea comprada a un precio superior si continúa cotizando a una valoración demasiado baja.

Conclusión:

El precio de la acción de PHINIA ha caído de $37 a $26.8 después del spin-off. Su capitalización de mercado es ahora de $1.2 billones, y su valor de empresa es solo 3.5 veces el EBITDA ajustado de 2022. Esto significa que el programa de recompra anunciado por la compañía en agosto representa casi el 12% de la capitalización de mercado, con el dividendo trimestral de $0.25 por acción agregando otro 3.8% a los retornos de capital. A este ritmo, y con el equipo directivo comprometido a maximizar los retornos para los accionistas, PHINIA tiene la capacidad de generar casi el 50% de su capitalización de mercado en flujo de caja libre de aquí a 2025.

Recursos adicionales:

Página de relaciones con inversores de PHINIA: https://investors.phinia.com/overview/default.aspx

Presentación de la presentación de resultados del Q2 2023 de PHINIA: https://s202.q4cdn.com/197651336/files/doc_presentations/2023/08/Q2-2023-Earnings-Call-Presentation.pdf

Formulario de registro de PHINIA: https://d18rn0p25nwr6d.cloudfront.net/CIK-0001968915/8e9a4d91-ba79-4eda-9b6c-fdbea7a5e222.pdf

Para mayor contexto sobre las expectativas de crecimiento en la flota global de vehículos híbridos recomendamos los artículos de The PeachPit sobre PHINIA y de Conor Maguire (no sabemos de qué empresa habla, ya que no estamos sucritos, pero el contexto sobre la dificultad de reemplazar la flota global de vehículos de combustión interna por una de vehículos eléctricos nos parece muy apropiada para nuestra tesis en Phinia):

Phinia Inc

A “boring” company in an unpopular industry that could return 100% of its market capitalisation to investors in just a few years.

David Einhorn, Chairman of Greenlight Capital, has been making the same point in nearly every interview he has given in recent years.

In response to how the asset management industry has changed over the past decade—during which the growth of passive strategies has pushed out almost all valuation-focused investors—Greenlight Capital no longer expects the market to recognise or re-evaluate the undervalued companies they invest in. Instead, Greenlight is much more focused on what the companies themselves can pay to Greenlight.

David has concluded that for some of these stocks, nobody is paying attention. Nobody is doing the work, nobody cares what the company says. Simply put, nobody is listening. Consequently, Greenlight Capital has restructured its portfolio so that, at least in theory, they can generate returns on their investments based solely on what the companies can pay them, rather than relying on other investors.

In a recent Colossus podcast, David said:

“We used to be able to buy things and say, "Well, this is an okay company and it's at 11x earnings, but I think that the earnings are going to be 10% more over a year or two or maybe 20% more, and it will get re-rated then to 15x earnings because people will see that it's better than they thought, so the stock will go up 60% to 80% over a couple of years, then it will be fully appreciated and we'll move on to the next thing."

The problem now is if you buy that thing, even if it plays out the way it does, if it started at 11x, earnings in two years, it's very likely, instead of being at 15x earnings, feels like it's going to be at 7x earnings. We're basically at the same price with earnings up 40% over a couple of years. And you're not really going to make any money because there's nobody who is appreciating what is going on and analyzing it. It just gets lumped into a bucket.

So we need to have that story combined with, well, instead of paying 11x earnings, we're going to pay 4x earnings. And we're going to pay 4x earnings, and there's going to be a 20% buyback going on. And I think if we're able to do that. And we can do that because there's really nobody paying attention, so there are plenty of companies that are actually that cheap.

Like, you say, "Well, where do you find companies are that cheap?" There actually are companies that are that cheap in unpopular areas that don't even necessarily have bad businesses. And I think we're going to earn our returns off of buying things at much, much lower values and holding them until the capital has been fully returned.”

The idea we present today might be a similar case.

Introduction and Investment Thesis

On 6 December 2022, BorgWarner (NYSE: BWA; market capitalisation USD 7.8 billion) announced plans to spin off 100% of the shares of its Fuel Systems and Aftermarket business under the corporate name PHINIA Inc. (NYSE: PHIN; market capitalisation USD 1.2 billion).

Through this transaction, BorgWarner aims to advance its goal of becoming a market leader in electric vehicle propulsion technology, while PHINIA will focus on its core business of manufacturing fuel systems and selling aftermarket parts.

In simple terms: BorgWarner expects the market to value it at a higher multiple by shedding the “heavy” exposure of PHINIA to internal combustion engines, which are so widely disliked by the market.

The truth is that as separate companies, both businesses will benefit from a more focused strategic approach and the flexibility to pursue their differentiated market opportunities.

As often happens with spin-offs, BorgWarner shareholders who received PHINIA shares opted to sell them immediately and indiscriminately in the public market, sending the share price plummeting to a low of $26.27 from its market debut price of $37. Owning shares in a smaller company exposed to internal combustion engines simply doesn’t align with the investment objectives of many BorgWarner shareholders, including many index funds.

We disagree with the prevailing narrative about the imminent demise of internal combustion engines and believe the current enterprise value of just 3.5 times trailing twelve-month EBITDA is unjustifiably low.

Business Overview

PHINIA is a manufacturer of fuel systems and a distributor of aftermarket parts. PHINIA’s product portfolio includes electric starters and alternators for engines, canisters that capture fuel vapours before they escape into the atmosphere, as well as injectors, pumps, and delivery modules for diesel, petrol, and alternative fuels like hydrogen, ethanol, and natural gas.

PHINIA’s fuel systems and aftermarket solutions enable internal combustion engines to operate at peak performance, optimising output, increasing efficiency, and reducing emissions.

PHINIA’s products are used in commercial vehicles and industrial applications (medium- and heavy-duty trucks, buses, and other off-highway construction, marine, agricultural, and industrial uses) and light vehicles (passenger cars, trucks, vans, and sport utility vehicles).

PHINIA believes its aftermarket segment (~38% of total 2022 sales) provides a stable, recurring revenue base, as the replacement of many of these products is non-discretionary by nature (if your starter system breaks, it’s hard to delay the repair). Additionally, they believe (and we agree) that the growing number of vehicles on the road, coupled with the increasing average age of vehicles and rising miles driven, will lead to growing demand for their aftermarket products.

In 2022, PHINIA derived 39% of its revenue from Europe, 41% from the Americas, and 20% from Asia. Furthermore, 27% of its net sales in 2022 came from commercial vehicle and industrial applications, 46% from light vehicle manufacturers, and 27% from aftermarket customers.

In 2022, General Motors accounted for 12% of net sales, with no other customer representing more than 10%. Its top five customers accounted for approximately 32% of net sales.

Breakdown of 2022 Sales by Geography, Segment, and Customer Type:

The Aftermarket segment generates a higher margin than the Fuel Systems segment. The following table presents the Net Sales and Adjusted Operating Income by segment:

Financial Analysis

PHINIA released its second-quarter results on 7 August 2023 and is scheduled to present its third-quarter results on Monday, 6 November 2023.

For the second quarter, PHINIA achieved year-over-year sales growth of 11.4%, reaching $887 million. This growth was higher than anticipated going forward as it included price increases negotiated with customers outside of contracts to recover the prior year’s inflationary material cost impacts. Moving forward, we expect an annual growth rate of 1-2%. This is definitively not a high-growth business.

The company also reported operating income (EBIT) of $56 million and adjusted EBIT¹ of $94 million, resulting in an operating margin of 6.3% and an adjusted operating margin of 10.6%, representing improvements of 10 basis points (bps) and 180 bps, respectively, compared to the prior year. Margins also benefited from inflationary cost recoveries retroactively applied to the beginning of the year. Corporate costs were also lower in the second quarter compared to the prior year.

Net income for the second quarter was reported at $35 million, with a net margin of 3.9%, and adjusted EBITDA was $130 million, resulting in an adjusted EBITDA margin of 14.7%, a 140-bps improvement from the previous year.

In its August presentation, the company reaffirmed its full-year 2023 guidance, expecting sales between $3.45 billion and $3.55 billion, adjusted EBITDA of $485 million to $505 million, and adjusted EBITDA margins of 13.8% to 14.3%.

Also in August, PHINIA announced that its Board of Directors approved a quarterly cash dividend of $0.25 per common share (a dividend yield of approximately 3.8% at the current share price). Additionally, the Board authorised a $150 million share repurchase programme, representing approximately 12% of the company’s market capitalisation.

Brady Ericson, President and CEO of PHINIA, commented:

“We are pleased to initiate a competitive quarterly dividend and a share repurchase program as we are confident in our business’s strong earnings and cash generation ability. We believe that our dividend, combined with opportunistic share repurchases, are the logical next steps in enhancing shareholder value. We remain committed to returning a substantial portion of free cash flow to shareholders, maintaining our strong balance sheet, making prudent organic investments, and selectively investing in rapidly accretive and high ROIC acquisitions. Our investments in the business will support our objective of sustainable profitable growth.”

One aspect we always appreciate in our investments is the alignment of management's interests with those of minority investors. According to BorgWarner's compensation policy, which PHINIA plans to maintain going forward, executives are expected to have a significant interest in the company through stock ownership. For the CEO, this means maintaining a stock position worth six times their annual base salary. As of 22 September 2023, Brady Ericson, President and CEO, held 401,837 shares with a total market value of USD 10.8 million (approximately 12.4 times his base salary).

We know he purchased at least 13,194 of these shares on the open market in August at an average price of $29.11, for a total value of $384,077. Beyond these purchases, we suspect that most of his remaining shares were granted as part of his compensation package rather than being purchased outright with his own personal funds. While it would be preferable to see the CEO buying shares using his personal wealth, his current stake in PHINIA represents a substantial amount relative to his base salary, aligning his interests with those of other shareholders. Indeed, he is the largest individual shareholder and the 11th largest investor overall.

Additionally, in the most recent analyst earnings call, Ericson mentioned plans to reset the company’s long-term incentive plan metrics, focusing on economic value, return on invested capital (ROIC), and overall cash generation of the business. We view these as positive objectives and look forward to seeing the plan’s details.

Market Analysis and Valuation

PHINIA’s competitors—including American Axle & Manufacturing, Dana, Magna, Vitesco Technologies (recently the subject of a takeover offer from Schaeffler with a premium of approximately 25% at the time of the announcement), and Tenneco—trade at a 5.0x EV/EBITDA multiple. This is significantly higher than PHINIA’s 3.5x multiple, despite PHINIA having a considerably higher EBITDA margin, better cash flow conversion, and lower leverage.

This valuation discrepancy suggests a compelling opportunity, particularly if PHINIA can demonstrate continued operational efficiency, cash generation, and alignment of management incentives to deliver shareholder value.

Simply applying this conservative EV/EBITDA multiple would imply a 60% increase in the current share price, without even accounting for the additional 15% capital return from dividends and share buybacks. Each additional 0.1x increase in the multiple would add approximately a further 4% increase to the share price.

Risks and Challenges

PHINIA is a smaller company compared to BorgWarner, which could lead to higher costs due to reduced purchasing power. Additionally, it may find it more challenging to maintain existing customer relationships and win new ones. When asked about this during the second quarter earnings presentation, CEO Brady Ericson responded:

“I think in general the way that things were set up under the prior ownership is most of our business units were pretty stand-alone. From finance, supply chain, engineering; our plants were pretty stand-alone. So from that perspective, there's not a lot different. There's obviously going to be some differences and the fact that legal, investor relations, treasury, tax are going to be some of the additional corporate costs that we need to add to our organization because that was some of the primary support that we had from our prior parent. So from our perspective that's going to be the biggest dissynergy.

With that said, I think we're going to be a lot more nimble in supporting our business and so I think we're going to be a lot more focused on our customers and our markets to help grow our business. And that's where I made the comment earlier around our customers are actually excited about the spin because they know they're going to have a trusted partner to supply them with combustion technology; whether it's carbon neutral, carbon-free, aftermarket parts for decades and decades. And so they were quite supportive and excited about the opportunity because they see us continuing to invest in that space and we're going to continue to help them transition to carbon-free fuels going forward.”

In other words, being smaller has some negative aspects but also certain advantages.

Another risk is PHINIA’s exposure to internal combustion engines. Beyond the risk of a faster-than-expected transition to electric vehicles (a view we do not share—we recommend reading the comments by PeachPit and Conor Maguire included at the end of this post), there is the fact that investors do not want to “touch anything” related to internal combustion engines. While this could lead to short-term selling pressure—and thus a buying opportunity for patient investors—it could also result in a permanent discount if the market refuses to properly value this business.

We believe the company’s focus on returning capital to shareholders through dividends and buybacks mitigates this risk.

We also believe the current multiple is excessively conservative given the historical multiples of comparable companies and see potential for this company to be acquired at a premium if it continues trading at an excessively low valuation.

Conclusion:

PHINIA’s share price has dropped from $37 to $26.8 following the spin-off. Its market capitalisation now stands at $1.2 billion, and its enterprise value is just 3.5 times its 2022 adjusted EBITDA. This means the buyback programme announced by the company in August represents nearly 12% of its market capitalisation, with the quarterly dividend of $0.25 per share adding another 3.8% to capital returns. At this pace, and with the management team committed to maximising shareholder returns, PHINIA has the potential to generate nearly 50% of its market capitalisation in free cash flow by 2025.

Additional Resources:

PHINIA Investor Relations Page: https://investors.phinia.com/overview/default.aspx

PHINIA Q2 2023 Earnings Call Presentation: https://s202.q4cdn.com/197651336/files/doc_presentations/2023/08/Q2-2023-Earnings-Call-Presentation.pdf

PHINIA Registration Document: https://d18rn0p25nwr6d.cloudfront.net/CIK-0001968915/8e9a4d91-ba79-4eda-9b6c-fdbea7a5e222.pdf

For further context on hybrid vehicle fleet growth expectations, we recommend the following article by Conor Maguire (while the specific company discussed is unclear to us since we are not subscribers, the context on the difficulty of replacing the global internal combustion engine vehicle fleet with electric vehicles aligns well with our thesis on PHINIA): EV transition on ICE? - by Conor Maguire

El EBIT y el EBITDA ajustado excluyen gastos relacionados con fusiones, adquisiciones, desinversiones, reestructuraciones y amortización de activos intangibles, y revierte los ingresos por regalías recibidos de BorgWarner que no continuarán en el futuro según los acuerdos de spin-off. / The adjusted EBIT and EBITDA exclude expenses related to mergers, acquisitions, divestitures, restructuring, and amortisation of intangible assets. Additionally, they reverse royalty income received from BorgWarner that will not continue in the future under the spin-off agreements.