Update Dowlais PLC: Un asalto más (English version at the end)

¿Puede estar un empresa barata, eternamente barata?

Como en las películas donde Michael J. Fox viaja al pasado, y está a punto de modificar para siempre el continuo espacio-tiempo…pero al final vuelve a un presente casi inalterado; tras un terremoto en la acción, Dowlais se encuentra cotizando en los mismos niveles de nuestra publicación de julio:

En este periodo de 6 meses, la compañía llegó a desplomarse un 30%, y alcanzar mínimos históricos en noviembre, para rebotar más de un 40%.

Un entorno débil para el sector, junto a unos resultados del primer semestre por debajo de expectativas en la división de autos, dieron lugar a una rebaja del guidance 2024.

Aunque no todo fue negativo en la publicación. La división de Powder Metallurgy tuvo un trimestre fuerte con unos márgenes operativos del 9.5% vs 9.2% del 2023 . Y con un interés creciente en imanes. El proyecto, que por ser una pieza clave para los coches eléctricos, tendría un componente de fuerte crecimiento.

Posteriormente ya en el trade update de noviembre se volvió a confirmar el guidance y que posiblemente ya habíamos visto el suelo, lo que dio a lugar a que las acciones llegasen a subir un 12% durante la sesión:

https://www.dowlais.com/files/investors/Results/2024/Dowlais-November-2024-Trading-Update.pdf

Pero lo más importante y por lo que volvemos a enviar material, es que Dowlais reportó que ha iniciado un proceso de revisión estratégica de la división de polvos de metalurgia, con la posible venta total. Incluso fue filtrado por Megermarket que Rothschild ya está al cargo del proceso con un mandato previsto para el 2025.

Fuente: Trading update noviembre 2024

Y aquí entra lo bueno y lo que a nosotros nos atrae como el imán al metal: antes teníamos una situación especial de infravaloración por Spin off, y ahora se le suma un posible mandato de venta de una división como catalizador grande. Tan grande como que pesa solo ~20% sobre las ventas y ~27% sobre el Ebit, pero que según Dowlais, al menos valdría £900m, es decir, lo mismo que capitaliza la compañía entera.

¿Cuánto vale realmente PM?

Si nos remontamos a 2018, ya estuvieron a punto de vender esta división al recibir una oferta de Apollo y PAI Partners por £1.6b, y que fue rechazada, al pretender una valoración de £2b. Desde luego, una mala decisión vista con los ojos de ahora.

Dentro del sector de Powder Metallurgy: Dowlais es el número 2 por cuota de mercado (24%) en metalurgia de polvos y el líder en producción de componentes sinterizados (13%).

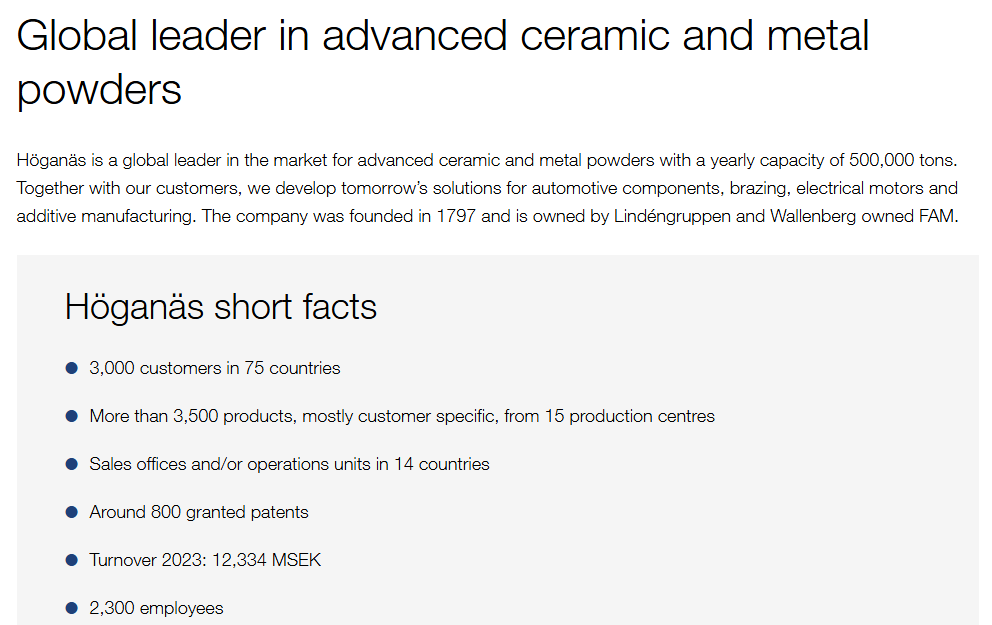

El líder mundial en metalurgia de polvos es la empresa sueca Hoganas que tras cotizar en la bolsa fue privatizada en 2013 a un múltiplo estimado ~10x EV/EBITDA, lo que equivaldría a ~£1.300m de equity value para PM de Dowlais.

Fuente: https://www.hoganas.com/en/about-hoganas/hoganas-in-three-minutes/

Lejos de las cifras de 2013 o 2018, el rango de aspiración del Management podría estar próximo a una cifra de £864m, que corresponde con la valoración en libros y que fue recientemente revisada a la baja mediante un impairment de £449m.

Fuente: presentación de resultados del ejercicio 2023

En nuestra entrada anterior ya estimamos para esta división una valoración suelo de £500m equivalente 0.5x Prite to Book. Y aunque se puede considerar que el negocio de combustión (50%) podría estar en run-off…ya veremos si es así, y en cuanto tiempo, lo cierto es que ya en 2023 la proporción de nuevas órdenes es en un 72% exposición a negocios diferentes de motores puramente de combustión, lo que poco a poco debería ir rebajando el mix de ingresos asociados a motores ICE de alrededor del 50%.

Fuente: presentación de resultados del ejercicio 2023

Pensamos que por la capacidad de generar caja de esta parte legacy, y el negocio de crecimiento, que incluye el desarrollo de la parte de imanes, PM de Dowlais podría tener interés tanto para fondos Private Equity que persigan un LBO y una posterior estrategia de consolidación, como para alguna compañía de aleaciones donde puedan encontrar sinergias.

El escenario Alternativo: ¿Que pasaría si esta compañía se mantiene barata para siempre?

En nuestra tesis de Phinia, a causa de un plan agresivo de reparto de caja al accionista, la cotización hasta ido escalando hasta estar ahora un 80% por encima del momento de la publicación.

En el caso de Dowlais podría ser todavía mejor. En la tesis inicial ya hablamos del potencial de generación de caja de la compañía y del plan de reparto al accionista entre dividendos y recompras. Y ahora nos encontramos con que, de conseguir vender la división de PM por £500m, y poder realizar un plan de recompras a estos niveles, es tan igual de poco probable que la acción sea inmune a… que no llueva en un año en Pontevedra.

Recapitulemos en detalle:

Este sería la política de asignación de capital de la compañía:

Fuente: Capital market event enero 2023

Consiste principalmente en destinar el exceso de cash a mantener niveles de deuda entre 1.0x - 1.5x (excluyendo los pasivos por pensiones), y retornar a los accionista cualquier posible desinversión.

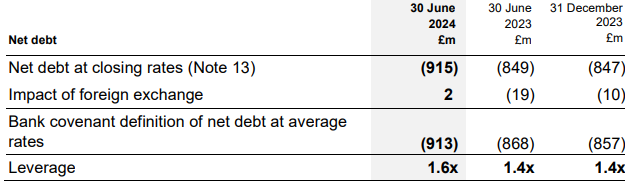

Aquí podemos comprobar la deuda, según la última presentación de resultados:

Fuente: presentación de resultados del primer semestre de 2024

La deuda neta a cierre de junio de 2024 era de £913m con un ratio en el rango alto de la compañía en 1.6x.

Si se produce la transacción y finalmente venden la división de PM, tendríamos que hacer dos ajustes:

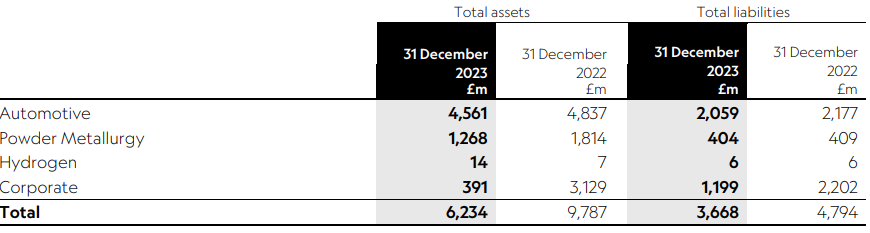

1) Descontar la deuda asociada a esta división: Aunque reportan liabilities de £404m, estimamos que ~£230m podría ser solo deuda financiera. La deuda neta pasaría de £913m a £683m.

Fuente: presentación de resultados del ejercicio 2023

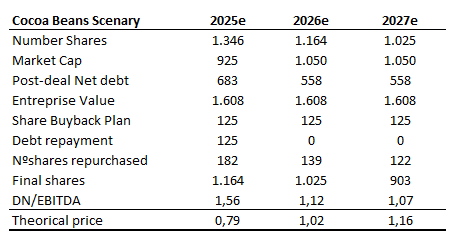

2) Ajustar el nuevo ratio DN/EBITDA sin la aportación de PM: Ebit ~£90-100 y con una amortización media de £50m, llegamos un Ebitda ex PM de £437m y un ratio de 1.56x.

Fuente: Elaboración propia

¿Cuál sería entonces la creación de valor?, si..:

Venden la división por £500m (EV de £730m)

De estos, se destina el 25% o £125m a la reducción de deuda para mantener el ratio DN/EBITDA en línea.

Se establece un plan de recompras con el montante restante de £375m distribuido en al menos 3 años.

La compañía consigue recomprar acciones sin re-rating de múltiplos (raro, raro..).

Fuente: Elaboración propia

Solo con el aumento del valor del equity a consecuencia de la reducción de la deuda, y de poder recomprar toda esa cantidad de acciones, el valor teórico llegaría a ser de un 70% por encima de la cotización actual.

Y no hemos añadido un muy probable mayor montante en recompras por la mayor generación de caja prevista para los próximos años: turn around realizado con 200pb de mejora de márgenes, o la venta de la división de Hidrógeno que drenaba unos 15m de caja.

Conclusión

En estos momentos el sector es tan popular como los periódicos de papel. No genera mucho entusiasmo. Sin embargo, vemos poco probable que este tipo de compañías se mantengan eternamente baratas. En este caso, es evidente que si se cumple la voluntad de la dirección de reparto al accionista, dadas las múltiples opciones: mejora los márgenes, venta de la división de PM, es poco probable que la acción no reaccione.

Y si no…siempre nos quedará una operación corporativa del grupo. Dentro del sector ya estamos viendo roedores en la debilidad. El principal accionista de Novem Group, ya anunció en octubre que estaban considerando una exclusión: https://www.bnnbloomberg.ca/investing/2024/10/02/billionaire-retail-clan-eyes-buyout-of-car-interior-firm-novem/

Y en España, estamos viendo como los dueños de Gestamp, están comprando acciones sin mesura:

https://www.eleconomista.es/mercados-cotizaciones/noticias/13130754/12/24/la-familia-riberas-roza-el-75-del-capital-de-gestamp-tras-la-ultima-adquisicion-de-tres-millones-de-acciones.html

Respondiendo a la pregunta del principio, ¿Puede estar una empresa barata, eternamente barata?.

Nosotros decimos…NEIN!

Dowlais PLC: One More Round

Can a company remain cheap, eternally cheap?

Like in the movies where Michael J. Fox travels to the past and is about to forever alter the space-time continuum... but in the end returns to an almost unchanged present; after an earthquake in the action, Dowlais is trading at the same levels as in our July publication:

During this 6-month period, the company plummeted by 30%, reaching historic lows in November, only to rebound by more than 40%.

A weak environment for the sector, along with first-half results below expectations in the automotive division, led to a downgrade of the 2024 guidance.

However, not everything was negative in the publication. The Powder Metallurgy division had a strong quarter with operating margins of 9.5% vs 9.2% in 2023, and with growing interest in magnets. The project, being a key component for electric cars, would have a strong growth component.

Subsequently, in the November trade update, the guidance was confirmed again, and it was suggested that we had possibly seen the bottom, which led to the shares rising by 12% during the session.

https://www.dowlais.com/files/investors/Results/2024/Dowlais-November-2024-Trading-Update.pdf

But the most important reason we're sending this material again is that Dowlais reported it has initiated a strategic review process for the Powder Metallurgy division, with the potential for a complete sale. It was even leaked by Megermarket that Rothschild is already in charge of the process with a mandate planned for 2025.

Source: November 2024 Trading Update

And here's the good part, and what attracts us like a magnet to metal: before, we had a special undervaluation situation due to the spin-off, and now there's the potential sale mandate of a division as a major catalyst. So significant that it accounts for only ~20% of sales and ~27% of EBIT, but according to Dowlais, it would be worth at least £900m, which is the same as the entire company's market capitalization.

How much is PM really worth?

If we go back to 2018, they were already close to selling this division after receiving an offer from Apollo and PAI Partners for £1.6b, which was rejected as they were seeking a valuation of £2b. Certainly, a bad decision in hindsight.

In the Powder Metallurgy sector, Dowlais is the number 2 by market share (24%) in powder metallurgy and the leader in sintered components production (13%).

The global leader in powder metallurgy is the Swedish company Hoganas, which was privatized in 2013 at an estimated multiple of ~10x EV/EBITDA, equivalent to ~£1.3 billion in equity value for Dowlais' PM division.

Fuente: https://www.hoganas.com/en/about-hoganas/hoganas-in-three-minutes/

Far from the figures of 2013 or 2018, the Management's aspiration range could be close to a figure of £864m, which corresponds to the book value and was recently revised downward through an impairment of £449m.

Source: 2023 Annual Results Presentation

In our previous entry, we already estimated a floor valuation of £500m for this division, equivalent to 0.5x Price to Book. And although it can be considered that the combustion business (50%) might be in run-off... we'll see if that's the case and how long it takes. The fact is that already in 2023, the proportion of new orders has a 72% exposure to businesses other than purely combustion engines, which should gradually reduce the revenue mix associated with ICE engines from around 50%.

Source: 2023 Annual Results Presentation

We believe that due to the cash-generating capacity of this legacy part and the growth business, which includes the development of the magnet segment, Dowlais' PM division could be of interest to both Private Equity funds pursuing an LBO and a subsequent consolidation strategy, as well as to some alloy companies where they could find synergies.

The Alternative Scenario: What if this company remains undervalued forever?

In our Phinia thesis, due to an aggressive cash distribution plan to shareholders, the stock price has been climbing and is now 80% above the publication time.

In the case of Dowlais, it could be even better. In the initial thesis, we already talked about the company's cash generation potential and the shareholder distribution plan through dividends and buybacks. And now we find that, if they manage to sell the PM division for £500m and can carry out a buyback plan at these levels, it is as unlikely that the stock will be immune to... as it is for it not to rain in a year in Pontevedra.

Let's recap in detail:

This would be the company's capital allocation policy:

Source: January 2023 Capital Market Event

It mainly consists of allocating excess cash to maintain debt levels between 1.0x - 1.5x (excluding pension liabilities) and returning any possible divestments to shareholders.

Here we can check the debt, according to the latest earnings presentation:

Source: H1 2024 Earnings Presentation

Net debt at the end of June 2024 was £913m with a ratio at the high end of the company's range at 1.6x.

If the transaction occurs and they finally sell the PM division, we would need to make two adjustments:

Deduct the debt associated with this division: Although they report liabilities of £404m, we estimate that ~£230m could be purely financial debt. Net debt would decrease from £913m to £683m.

Source: 2023 Annual Results Presentation

Adjust the new Net Debt/EBITDA ratio without the contribution from PM: EBIT ~£90-100 and with an average depreciation of £50m, we arrive at an EBITDA ex PM of £437m and a ratio of 1.56x.

Source: Own elaboration

What would be the value creation then, if..:

They sell the division for £500m (EV of £730m)

Of this, 25% or £125m is allocated to debt reduction to maintain the Net Debt/EBITDA ratio in line.

A buyback plan is established with the remaining £375m distributed over at least 3 years.

The company manages to repurchase shares without a multiple re-rating (rare, rare..).

Source: Own elaboration

Just with the increase in equity value as a result of debt reduction, and being able to repurchase all those shares, the theoretical value could be 70% above the current price.

And we haven't added a very likely larger amount in buybacks due to the higher cash generation expected in the coming years: turnaround achieved with a 200bp margin improvement, or the sale of the Hydrogen division that was draining about £15m in cash.

Conclusion

At the moment, the sector is as popular as print newspapers. It doesn't generate much enthusiasm. However, we see it as unlikely that these types of companies will remain perpetually undervalued. In this case, it is evident that if the management's intention to distribute to shareholders is fulfilled, given the multiple options: margin improvement, sale of the PM division, it is unlikely that the stock will not react.

And if not... we will always have a corporate operation of the group. Within the sector, we are already seeing opportunists in the weakness. The main shareholder of Novem Group already announced in October that they were considering a buyout: link

And in Spain, we are seeing how the owners of Gestamp are buying shares without restraint: link

Answering the initial question, can a company remain cheap, eternally cheap?

We say... NEIN!

| Una publicación invitada por

|

Muy buen update! Comentar que actualmente ya están ejecutando un programa de recompras de 50 millones. En H1 usaron unos 9 millones y en H2 y lo que llevamos de 2025 han recomprado día si día también. Calculo que podría estar sobre las 1.290 m. acciones al terminar.