Buffett's presentation at Sun Valley in the midst of the tech bubble

Mistakes and successes in 2024

"A good investment is never easy, and an easy investment, by definition, cannot be good." Fernando Bernad Marrase (Azvalor Asset Management)

In July 1999, Warren Buffett gave a speech about the state of the markets at Sun Valley. It can be found almost in its entirety in Chapter 2 of the authorized biography of Buffett, The Snowball. This part of the book is titled, The Bubble.

Sun Valley is like an annual conclave of business celebrities, in Buffett's words, “you get people to come because attending a meeting of elephants assures them that they are one too”.

This talk took place at the peak of the tech bubble, a time when the valuations of tech companies and 'old economy' businesses diverged dramatically. Warren Buffett delivered one of the keynote speeches, which was quite provocative and has been widely quoted.

Let's take a look at the first slide he showed:

Dow Jones Industrial Average

December 31, 1964: 874.12

December 31, 1981: 875.00

"Over these seventeen years, the size of the economy quintupled and the sales of the Fortune 500 companies grew more than fivefold. However, during these seventeen years, the stock market went nowhere”.

He then went on to discuss the revolutionary inventions of that era to draw a comparison with the current revolution of the internet and e-commerce.

About automobiles: “This is half a page from a list of seventy pages of all the automobile companies in the United States!' There were two thousand automobile companies: probably the most important invention of the first half of the 20th century. It had a huge impact on people. If you had seen at the time of the first cars how this country would develop in relation to cars, you would have said: 'This is the place to be!' But of the two thousand companies, from just a few years ago, only three automobile companies survived. And at one time or another, all three were selling for less than their book value. So cars had a huge impact on America, but in the opposite direction for investors."

Regarding airplanes: “The other great invention of the first half of the century was the airplane. In this period from 1919 to 1939, there were about two hundred companies. Imagine if you could have seen the future of the 1 aviation industry, you saw all those people who wanted to fly and visit their relatives or run away from their relatives or whatever you do in a plane. That's where you had to be.' 'For a couple of years, none of the investments in airlines have yielded a single dollar”.

Among the attendees were the main figures of the tech companies of the moment, such as Bill Gates, who, although it couldn't be known at the time... Microsoft, months later, reached a stock market peak whose maximum would not be recovered until almost 17 years later in 2016.

At that time, Buffett's credibility was questioned for the first time, and articles could be seen like the one we share below from one of the main economic publications with covers that, in time, proved to be prophetic of a debacle.

Source:https://www.barrons.com/articles/SB945992010127068546

Now we know what happened months later: the tech-heavy Nasdaq corrected 75% between March 2000 and September 2002, while Warren's holding company, Berkshire Hathaway, went up 40%.

Entering 2025

Almost a quarter of a century later... the same Buffett has the highest percentage of liquidity in his history in absolute terms and a relative level similar to that of 1999.

It's funny, but just a few months ago The Economist published an article with this cover:

We may not be worthy of emulating the great master, but we could make an almost perfect analogy of that old talk with the current fashion index, the S&P 500.

S&P500

March 24, 2000: 1,527.46

May 5, 2007: 1,530.23

This period coincided with the economic boom prior to the financial crisis, but the stock market didn't go anywhere in those 6 years. Subsequently to that almost punctual peak of 2007, came the financial crash, so in practice the 2000 highs weren't recovered until February 19th, 2013.

Summarizing: just like Warren's transparency, and despite the good macroeconomic figures, anyone who invested in the S&P 500 in 2000 didn't start making money until 12 years later.

The topic of the moment... Artificial Intelligence.

According to Stanford University's 'Measuring trends in AI' report, there are 5,509 AI startups in the United States alone, and in 2024, 43% of new unicorns, that is, new companies valued at over $1 billion, are AI companies.

Moreover, in any casual conversation, and not so casual... in the most professional circles of equity investment, everyone is clear that artificial intelligence is “where you need to be now”.

The risk is at the starting point

Valuation and expectations... it's always the same.

No matter how you look at it, the US stock market is expensive and at 1999 valuation levels (multiples), and we are aware that the quality of today's technology businesses is extraordinary. Despite this, the risk is always at the starting point and at the time of entry.

In Warren's example, it took 17 years to recover the 1964 peak of the Dow Jones, and in the more recent case of the S&P 500, it took 12 years between 2000 and 2013. Even the recent peak of 2021 in the S&P 500, after the growth stock bubble, has only recently recovered in 2024.

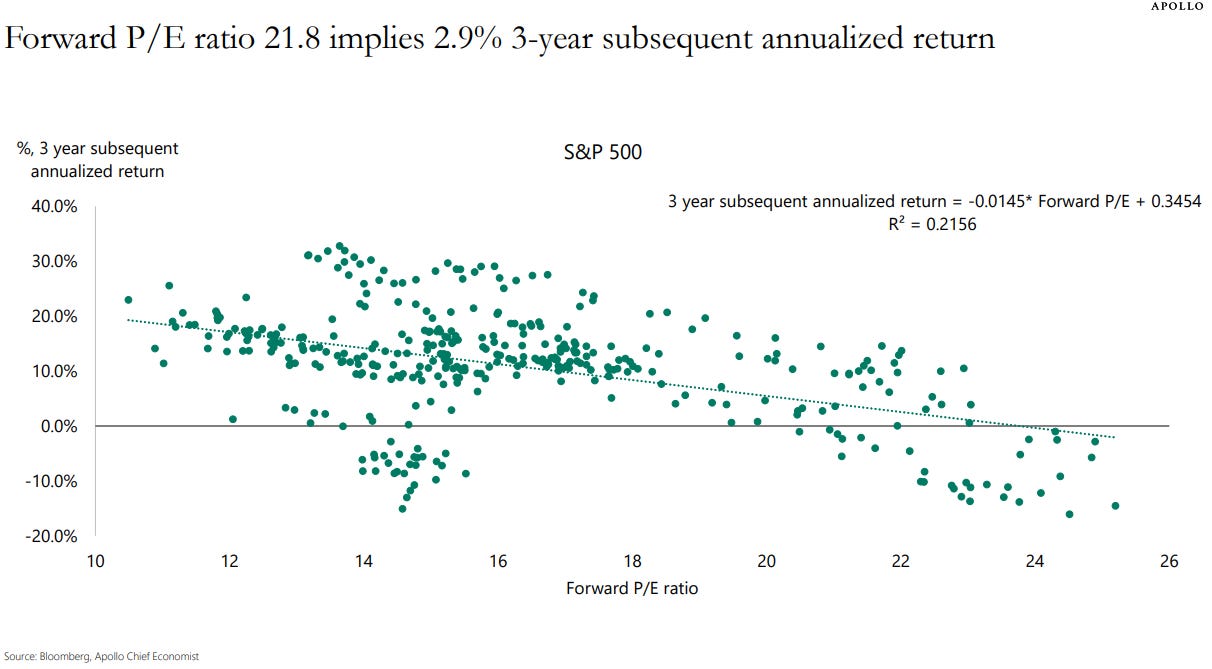

In a much more quantitative way, Apollo published a graph a few weeks ago: it consists of a regression of the expected return on the S&P 500 for the next three years based on its historical average valuation. It means how much has been obtained on average in the stock market, depending on its valuation at the time of entry.

The expected return of this inference is 2.9%, compared to a Treasury bond that would be approaching 5%.

We have nothing else to add. We don't know if the S&P 500 is going to correct in 2025 and then rebound in a V-shape or if it's going to remain flat for another 12 or 17 years, but what we do believe is that the risk/return would not be rewarded at this time. And that it is time to avoid it. At least if you want to obtain higher returns, and in our opinion, in a safer way.

The good news is that the divergences between what is expensive and cheap, or big or small, American or Chinese/European are enormous.

Fortunately, we have not stopped finding special situations during this 2024, many of them published right here.

Ideas assessment: Successes and Failures

SUCCESSES:

NH HOTELES

Our flagship idea, where we predicted that Minor, with a 96% stake in NH, would likely launch a squeeze-out takeover bid for the remaining 4% at a price at least 50% higher... and it has come to pass. The result has been a 66% return for this idea.

Phinia INC

Special situation with a spin-off inefficiency and book oversell. We titled the idea: 'A boring company in an unpopular industry that could return 100% of its market capitalization to investors in a few years'. Today, the price is 80% above the publication price.

Societe Fonciere Lyonnaise SA

French REIT owned 98% by the Spanish REIT Colonial. In this publication, we wanted to highlight that the price had returned to levels similar to the previous takeover bid. Additionally, we found that the timing was perfect because interest rate prospects were already on the decline, and this is one of the main drivers of the sector. Finally, in November of this year, Colonial issued a statement with the intention of excluding it. Pending the final exchange price, SFL is 9% above the price of our publication. We believe there is still some arbitrage opportunity.

Liberty Global Ltd

One of the most exciting ideas we discovered. A holding company with a treasure trove of assets, a management team that reinvented the game, conducting massive buybacks with a value unlocking plan. We said we saw a very feasible return similar to that achieved in Elecnor in 2023, which was around 50% in just 3 months. Today, the total return of the operation is 25%, but we still expect much more from this idea.

Zegona Communications PLC

Our newest and most promising idea. A tremendously interesting situation worthy of a business school case study. If everything goes according to plan, it could be a potential multi-bagger. Since we published it, exactly one month ago, the return on this idea has been 31%.

Prosegur y Prosegur Cash SA

Double-sided idea centered around a takeover bid launched by the controlling family for a percentage of Prosegur. On one hand, we explained how one could safely earn around €765 in a couple of months by buying Prosegur shares. On the other hand, we believed that this takeover bid could trigger another squeeze-out offer for Prosegur Cash by the parent company. Although that squeeze-out offer hasn't happened (yet), the return on this idea is 26% between capital appreciation and dividends, which is similar to what we estimated if our premise was correct.

High Arctic Energy Services

This was the first idea we published on Cocoabeans. A micro-cap company with reorganization plans including a spin-off and a cash distribution to shareholders. When we published, the company was valued at CAD 1.34, they were going to pay a dividend of CAD 0.76, and we estimated that the rest of the business was worth at least CAD 1.31, meaning that all in all the company should be valued around CAD 2. Finally, they paid the CAD 0.76 dividend (tax-free) and spun off the company into High Arctic Energy and High Arctic Oversea. The price of the entire operation is 5.6% higher than the day of publication but reached a +30% peak in the days following the spin-off.

MISTAKES:

Alantra SA

Our most popular idea by number of views. Despite believing it's very cheap and we're at the bottom, we were a bit optimistic about the timing of the industry's recovery. However, we are seeing signs that there is a lot of money tied up in terms of M&A deals that are to come, possibly sooner rather than later, and we already mentioned in a second part that recoveries in this sector are explosive. We remain very excited about this idea at this price, 8% below our publication price. We leave this video presentation recorded in October with the Locos de Wall Street where we explain the thesis.

Believe SA

An idea where we tried to explain that a counter-offer could be made by Warner, forcing the current owners to potentially increase the price of the takeover bid made a few days earlier. Days after publication, Warner Music announced its withdrawal from the deal, and we quickly sent a note abandoning this idea. The operation resulted in a 5% loss on the publication price.

Dowlais Group PLC

Auto parts spin-off that fell 50% from its IPO price in 2023. Another classic example of an oversell due to a spin-off of a company in a sector without momentum. We published this idea and it fell 30% below our initial price before recovering to be only 2% below our price. After publication, they have announced that they will sell one of the divisions that the market dislikes the most and may possibly distribute a special dividend or make a massive buyback. If it does not end up rising to a price that is close to our target price, we think it will eventually be acquired.

Deoleo SA

Highly controversial Spanish company after undergoing several capital increases and a restructuring with a debt haircut and recapitalization where shareholders lost all their money. When we published the idea, the balance sheet was already healthy and the controlling shareholder intended to sell the company. After some purchase rumors, the operation is being delayed due to the sector having gone through the worst period of the century due to a series of droughts that have prevented normal harvesting. Logically, this has reduced the company's accounts, reducing visibility and therefore has affected any potential candidate in the sector, who could consider a purchase. We expect the operation to resume at any time, since the shareholder is a private equity with the intention of exiting. So far this idea has resulted in a 20% loss.

Syensqo SA

Spin-off trading below its IPO price. Szensqo is a quality company but within a sector (chemicals) with currently negative momentum. Since publishing the article in October, the stock has fallen 13%, but Syensqo has presented better-than-expected results in the third quarter, highlighting stability in material prices and volume growth (first quarter with growth after seven consecutive quarters of declines). Additionally, the company provided a free cash flow projection for 2024 in line with market expectations and announced a €300m share repurchase program, starting with an initial €50m phase on November 5th.

We are not changing a comma of this idea. Syensqo continues to trade at the lower end of its comparables, and we believe the thesis is intact.

We would like to extend our best wishes for a Happy New Year to our 600+ newsletter subscribers.

We hope this year brings you good health and numerous opportunities.

Sincerely, Cocoabeans podcast

Great update. Thank you very much!